Inside the Maple ($MPL) Pool Implosion

Is This the Death of CeDeFi?

This research memo is for educational purposes only and not an inducement to invest in any asset. Subscribe to Blockcrunch VIP to receive in-depth project analysis, interactive token models and exclusive AMAs from our research team - all for the price of a coffee ☕ a day.

In the aftermath of the fallout of FTX, more skeletons are falling out of the proverbial closet in crypto.

The latest one concerns a well-known trading firm in crypto, and DeFi darling Maple Finance. Orthogonal Trading, a trading firm based in Australia, has borrowed vast sums on uncollateralized lending protocol Maple Finance, and is now allegedly unable to pay back their loans, putting lenders at risk.

In a previous memo, we discussed how Maple represents the likely path for DeFi to scale by incorporating the efficiency of centralized lending desks in DeFi.

With the recent blow up, one is tempted to ask: is the CeDeFi thesis and/or Maple at risk? A broader question: if DeFi can’t reliably grow beyond its clunky, over-collateralized status quo without introducing more trust assumptions - what is the point of DeFi at all?

This week, we will examine:

How Maple Works - A Quick Recap

What Happened in the M11 Credit USDC Pool

Orthogonal Trading’s Impact on DeFi

Lessons for CeDeFi protocol Design

Impact for Maple Finance

Maple Rehashed

Previously, we prepared a 30-page memo explaining how Maple works. Below we provide a short recap:

What is Maple?

Maple is a protocol that allows people to do three things:

Borrow money from others;

Lend money to others, and;

Manage loans between the former two and earn a fee

How do users lend on Maple?

Users can deposit their capital into any of Maple’s pools by simply going to their website and depositing either USDC or ETH. Some pools are permissioned and require manual onboarding and KYC with the Maple team.

How do users borrow on Maple?

Borrowers on Maple submit a loan request, which is then subjected to diligence by the Pool Delegate, a third-party who manages the pool. This diligence typically involves reviewing the creditworthiness of the counterparty, after which the delegate will approve funds to be dispersed to the lender from the credit pool.

This process is opaque and lenders are effectively trusting the competency of pool delegates to ensure the security of the protocol. That being said, as the intention is for pool delegates to be voted in by a decentralized community of token holders in the long term, there is an argument to be made that this is a sufficient compromise between decentralization and efficiency.

What happens if someone can’t repay their loan?

Unlike other DeFi protocols like Compound or Aave, Maple loans are under-collateralized - which means trading firms that prioritize capital efficiency above all else are a natural user segment. While Maple has processed loans with up to 50% in collateral value (e.g. $50 in collateral for $100 borrowed), most of Maple’s loans are un-collateralized.

Loans are given out in fixed terms (e.g. 60 days, 90 days); if a borrower defaults and fails to repay, the only recourse is legal. In other words, if you’re a borrower who is unable to pay back a loan on Maple, you can expect a letter from the Pool Delegate and/or Maple’s foundation’s lawyers. Any recovered assets in a liquidation process will then be paid out to lenders in a pro-rata fashion alongside other creditors of the same seniority.

Now that we have the context, let’s dive into the weeds…

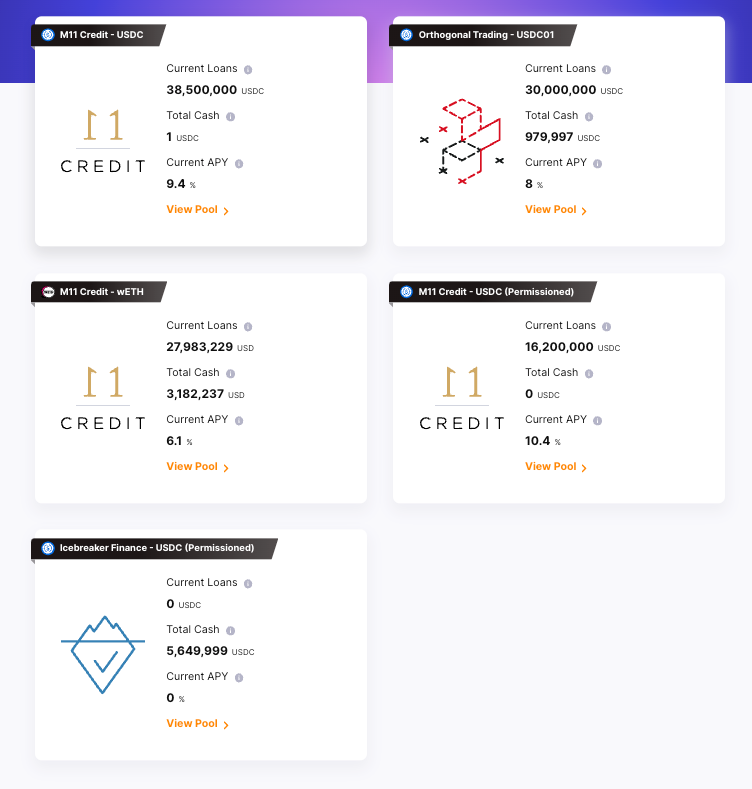

The M11 Credit USDC Pool

M11 Credit is a credit fund that manages multiple pools on Maple - in fact, they have had a stellar track record in navigating credit risks to date on Maple.

One of the pools managed by M11 Credit is the M11 Credit - USDC pool, which allows users to borrow and lend USDC. From inception to date, the pool has originated over $596M in loans with an average tenure of 140 days. As of October 1st 2022, the pool has generated $731,309 in interest for lenders, with an average interest rate of 10.76%.

In other words, the pool has functioned profitably for both M11 and lenders, with no incidents…till today.

So what went wrong?

Mounting Troubles

As of June 2022, M11 Credit was operating a reasonably healthy USDC pool - with $244M in outstanding loans, 12 different borrowers, with no single borrower taking up more than 15% of the pool in loan volume. Most of the borrowers were also market makers, which tended to imply neutrality in market bias (meaning price movements should not impact their solvency).

However, as of October 1 2022, a dramatic change happened that went largely unnoticed: while the gross loans have fallen from $244M to $105M, the number of borrowers went down to 5, and the share of some of the borrowers became much larger than the 15% cap.

For instance, market maker Wintermute was ~42% of the loan origination, and Orthogonal 26%.

While this might make prudent lenders cringe, all could be well as long as market makers remain solvent. Wintermute and Orthogonal are familiar names within crypto, which likely meant they have weathered enough volatile cycles to at least have some semblance of risk management.

However, with the FTX scam officially imploding, this began to change for Orthogonal Trading.

Background on Orthogonal Trading

To understand how Orthogonal could have collapsed, it’s helpful to understand what they do.

Joshua Green, Managing Partner at Orthogonal, is widely known as “Convex Monster” or “CM” on Twitter - an active trader with a wide following. Green and Orthogonal are known to be active participants in DeFi.

Namely, CM managed a fund on dHedge, a protocol for retails to invest in fund managers usually reserved for accredited investors. The fund is currently -65% year-to-date, with the last trade made around 7 months ago. Given the size of the fund ($132K) it was unlikely that this was material in any way for Orthogonal’s insolvency…moving on.

CM was also known to be the founder of Horizon Finance, a protocol that was launched in Q4 of 2020. The protocol purported to offer interest rate swaps for a wide variety of assets. However, given the complete lack of development over 2 years, the project was eventually shutdown. As Green raised external venture capital from Alameda, Framework Ventures, DeFiance Capital, Mechanism Capital, Spartan Capital and others, it was unlikely to have had any impact on Orthogonal’s solvency.

As part of their DeFi efforts, Orthogonal also served two functions on Maple Finance - as a manager of a credit pool with ~$30M in loans, and a borrower from other pools, notably the ones managed by Europe-based fund Maven 11’s Credit Team, mainly the USDC pool.

FTX Implosion and Orthogonal Cover Up

For readers who would like to revisit the FTX event, we wrote a comprehensive explanation of events that led up to FTX’s collapse earlier last month. Note that the following portion is simply educated conjecture based on multiple chats with parties involved in the incident - the official facts remain to be disclosed.

While market makers should theoretically be delta-neutral, if counterparty risk is not managed well this can change very quickly. This was possibly the case for Orthogonal - who was likely hedging some of its exposure on FTX when the exchange was revealed to be insolvent and froze withdrawals. It is possible that Orthogonal was hedging its long exposure on FTX, the implosion of which forced its entire exposure to skew heavily long in a downtrending market.

This has two consequences:

Orthogonal’s assets under management took a large hit from FTX insolvency

Orthogonal’s long exposure (assuming not unwound quickly) took a hit as markets are sold down

The above two could quickly render any fund insolvent - even by and large delta-neutral one, let alone one that seems to have strong directional views as evidenced on Twitter.

In an ideal world, this would be communicated clearly to counterparties (i.e. M11 Credit team), who can then assist with an orderly liquidation process, or perhaps a re-negotiation of loan terms. Instead, Orthogonal seems to have misrepresented their solvency to counterparties, leading to a $31M hole in the USDC pool, and $5M in the ETH pool, assuming zero recoverability.

As part of the recoverability process, the Maple Foundation, in conjunction with Maven 11 Credit, will likely pursue legal recourse against Orthogonal trading to attempt to recover assets for users, based on comments from the team.

As part of the revelation that Orthogonal Trading was likely fraudulently misrepresenting its financial position to M11 Credit over the past 4 weeks, the Maple platform has also decided to terminate Orthogonal as a Pool Delegate as well.

Lessons for CeDeFi

Relative to massive, centralized fraud (e.g. FTX), the Maple event is a drop in the bucket; however, the structural risks it reveals about CeDeFi are worth pondering for anyone with a long term stake in the future of DeFi.

It is important to note the silver linings as well: in a centralized context, it is likely that Orthogonal’s insolvency would lead to a collapse of all its businesses, from trading to credit. However, as funds are siloed in different smart contracts, Orthogonal Trading being insolvent actually does not hamper the activities of the Orthogonal-managed pool.

In addition, the ability for anyway to publicly audit outstanding loans and repayment history on Maple means that lenders already have a significantly higher level of transparency than they typically enjoy from massive, centralized lending desks (which seem to have been blowing up left and right as of late).

At the same time, CeDeFi builders and investors will be well-served to derive important lessons from the Maple incident. In our view, the following improvements should be high on Maple’s - or any CeDeFi under-collateralized lending protocols’ - priority list:

Advanced Risk Monitoring

For any protocol managing a portfolio of loans such as Maple, it is important to keep risk limits on each counterparty and be diversified against multiple forms of risk.

For instance, even if all of your counterparties are delta-neutral market makers by mandate - which should protect you against market swings - if all of them move their assets to one exchange which was subsequently revealed to be a giant Ponzi scheme, your entire loan portfolio can still go poof!

In risk assessment, requiring counterparties to share addresses, or read-only API-keys for centralized venues in order for pool delegates and lenders to monitor custodial concentration can be a serviceable solution.

For instance, Credora (disclaimer: Jason’s former employer, Spartan Capital, is an investor and Jason has small exposure via unvested carry from the fund) allows lenders and borrowers to monitor their risks in real time without revealing specific positions.

The main caveat here is that this is still a permissioned onboarding process - and unfortunately, Orthogonal was the only counterparty that refused to integrate Credora on Maple.

That being said, by refusing to lend to borrowers who are not integrated, CeDeFi can enforce a standard that mitigates such events in the future.

Loan Book Tenure Constructure

While M11 Credit did seem to have capped its counterparty risk for each borrower as of June 2022 to under 15% each, the disparity in loan tenure and the recent credit contraction introduced massive incentive problems into the system.

Namely, in times of heightened market risk and uncertain exchange security, borrowers hurriedly return their loans on Maple to either reduce their leverage, or to limit their exposure to other borrowers sharing the same pools.

However, as responsible borrowers hurry to reduce risk, those who are less responsible - even insolvent - are in no rush to do so. We see this in the case of the M11 Credit USDC pool: where the gross amount of loans drastically reduced (as borrowers return capital), directly resulting in the % share of less credit-worthy borrowers become unwieldy as Orthogonal goes from 8% to 80%.

As loans are fixed terms, there’s no real way to recall the loan from Orthogonal early to maintain exposure levels. On the lender side, those who sense issues arising with counterparties will also rush to the exits to withdraw, leaving those who are slow to do so exposed to a pool of borrowers with increasingly bad credit profile.

In other words, whoever is slow to withdraw in a Maple pool wherein one large borrower faces solvency issue will be left holding - theoretically - the biggest bag of odorous excrement ever assembled in the history of capitalism…ok, maybe not quite as bad (kudos to whoever got the reference)

One potential solution beyond a more sophisticated tiering of loan terms in a portfolio (which will STILL not resolve the issue if most borrowers decide to pull at the same time after a major market event…say, a major exchange turning out to be a Ponzi scheme) is the introduction of open term loans.

In fact, this is already planned in Maple v2, whereby pool delegates can force execute a loan recall. The borrower has 48 hours to return capital, or face liquidation procedures. This does not have the same guarantees as an auto-liquidated, over-collateralized DeFi loan, but is a step in the right direction.

Increase Insurance Alternatives and Diversify Borrower Profile

Currently, Pool Delegates are required to put up collateral to insure deposits in a pool - however, it’s easy to see how this can be burdensome should pools scale.

The result is only ~10% of Maple pools are insured by pool delegates, which in cases where a defaulting borrowers is 80% of the loan pool means “sorry, McDonalds for dinner hun” for lenders.

To cover for this, Maple currently allows users to stake Balancer Position Tokens (BPT) - a representation of a liquidity provider position in the MPL:USDC pool Balancer - to function as first-loss capital in return for a yield derived from interest and token inflation. This serves the dual function of incentivizing MPL liquidity as well. However, the pool currently consists of $4.5M only, which does not cover for majority of the assets in Maple.

Initially, Pool Delegates are required to stake $100,000 of BPT to initialize a pool. In the future, it makes sense for Maple to scale the required BPT stake from pool delegates commensurate with the size of the pool, enforced by a cap in loans that can be approved.

The lack of robust insurance is not idiosyncratic to Maple - for Clearpool, insurance is only up to 5% of assets. Likewise, TrueFi also uses its own native token as a form of first-loss capital and it’s easy to see why this will become a problem should the platform as a whole go under and investors lose confidence.

Without a clear path to more robust insurance, Maple could explore credit default swaps; however, it is not clear who the natural seller for said swaps are.

That leaves only one path forward: the aggressive diversification of borrower types to grossly minimize systematic risk, which may require Maple to venture beyond market makers - or even crypto.

Therein lies the challenge - without diversification, “mainstream” counterparties are unlikely to take a leap with DeFi; without them, there is no diversification.

A potential solution could be on-chain credit scores, which could happen 1 of 3 ways:

Create crypto-native credit scores. Projects such as Spectral, which allows you to combine several wallet profiles to construct a credit score based on your onchain history, are working on this. The pro: it’s easy; the con: it requires credit to be built up from 0

Bring off-chain credit scores on-chain. Oracle infrastructure can be repurposed for this. The pro: it allows institutions outside of crypto to borrow today; the con: it requires some centralized attestation to bring said data on-chain as such data is not publicly verifiable.

Offer non-crypto native borrowers loans on crypto. This is derivation of the first two - but by lending capital in a conservative manner on DeFi to e.g. a SME lending business or a FinTech business, a project can effectively kickstart the on-chain credit history of any entity, which opens up the path for unsecured loans. This is effectively the approach taken by projects like Teller.

Conclusion

All in all, for CeDeFi to progress, it must be a step function improvement over CeFi - not just an environment for looser credit conditions for degenerate gamblers.

It already has a few key pieces: most notably non-custodial loans and transparency in on-chain outstanding loans and credit history. However, much remains to be done in limiting the risk imposed by a largely homogenous set of counterparties in CeDeFi.

In the coming months, we expect to see a loss of confidence from lenders in loaning to crypto market makers and continued credit contraction in the space. However, our thesis remains intact for the need for a decentralized, transparent and safe way to transfer and transact value online - now more than ever.

The Blockcrunch Podcast (“Blockcrunch”) is an educational resource intended for informational purposes only. Blockcrunch produces a weekly podcast and newsletter that routinely covers projects in Web 3 and may discuss assets that the host or its guests have financial exposure to. Views held by Blockcrunch’s guests are their own. None of Blockcrunch, its registered entity or any of its affiliated personnel are licensed to provide any type of financial advice, and nothing on Blockcrunch’s podcast, newsletter, website and social media should be construed as financial advice. Blockcrunch also receives compensation from its sponsor; sponsorship messages do not constitute financial advice or endorsement.

Goes to show that the contagion stemming from FTX is going to take a while to flush out. I do think the Maple team is great and is handling it well. Looking for MPL price to stabilize and may end up picking up more.