The Definitive Post on the FTX Scandal

An Insider's Take of What Happened

Last week, I wrote a thread on the recent FTX saga that 12,000,000 of you read - including a certain meme-loving rocket scientist.

A few of you requested the thread in a more detailed and readable blog form, which I have created below for Blockcrunch VIPs.

Since then, a few more things have come to the light and numerous publications have reached out asking for clarification, including revelations that SBF’s lawyer terminating their partnership, his chief regulatory officer being tied to an online poker scandal, as well as the new CEO for FTX castigating SBF’s complete lack of internal risk oversight.

More is likely to surface, and I’ll leave the rest of this saga to journalists.

Below, I’ll share my account as an insider in the industry as to what led us to this point, which hopefully services as a cautionary tale for founders and investors for spotting future fraud. Most views are subjective and I have done my best to verify the veracity of each source and piece of “evidence”, but cannot guarantee 100% reliability as the event is still unfolding.

I have also shied away from the more salacious/ sensationalist aspects of the event and SBF’s personal life except for aspects that were directly relevant to the FTX implosion.

For those who want a 20-minute audio overview, you can check out our podcast here.

The Rise and Fall of FTX

The story of Alameda and FTX can best be summarized by SBF’s philosophy of betting big. Every major decision they have made is related to acquiring more leverage - via deceptive fundraises, financial engineering, and ultimately, outright fraud, as we will see below.

From Alameda to FTX

In Nov 2018 - Jan 2019, a small hedge fund called Alameda Research was raising debt from investors, promising "HIGH RETURNS WITH NO RISK".

At the time, Alameda Research allegedly had $5M in equity but were trying to borrow $200M at 15% APY to finance their market making activities, which they touted as extremely profitable.

Around that time, I met SBF in Macau at a crypto event - in what I believe was his first trip to Asia - as he was surveying whether to start his business here. Around that time, FTX planned a launch for July 2019 and closed a $8M seed from several funds, announced in August 2019.

In one investor's memo, "Alameda & FTX" is cited as a risk, as well as concerns around SBF’s personal split commitment between the two.

From my primary sources (who will remain undisclosed), FTX was allegedly started as an easy way to access capital by Alameda due to difficulties in raising for the latter. Below is an account from one of the first VCs that spoke to FTX - who revealed that Alameda was bleeding money to incubate FTX. At the onset, it seemed like Alameda and FTX’s ties were already quite murky:

In the early days, Alameda being a heavy portion of FTX's volumes was an open secret. Employees told me Alameda has an exclusive API key that allows faster access than any user - offering a systematic way to profit off clients. A message I sent to an FTX investor raising some oddities back in 2019 that highlighted the irregularity in FTX’s volume:

Ironically, I passed on an opportunity to invest in FTX’s very first round precisely because I thought having a market maker trade against its own clients on an exchange was unethical and potentially dangerous. Subsequently, I attributed this to one of the greatest misses of my career, and decided that Alameda was probably an unconventional but effective way to bootstrap liquidity on a new exchange.

I never predicted that FTX would balloon into the multi-billion dollar scandal that it was.

Bad Blood with Binance and DeFi Summer

Around September 2019, Alameda’s aggressive tactics were beginning to ruffle some feathers. They allegedly attempted to manipulate futures on Binance by crashing market prices on one of their contracts, but the attempt was thwarted by the latter.

However, this would likely mark the beginning of the bad blood between Binance and FTX that spelt the end for FTX.

As FTX continued to grow, its appetite for capital seems insatiable. In the midst of the so-called "DeFi Summer", FTX capitalized on the DeFi hype by creating Serum, a decentralized exchange on Solana. The raise was conducted in a way to encourage speed and not diligence - the faster investors committed, the lower the price.

Below is a screenshot of their fundraising tranches for Serum, with some investors getting a 50% higher price for committing a few hours later. I remember getting a message about this, and effectively given less than 24 hours to decide whether to write a check.

Obviously, we didn’t.

After, FTX became directly involved with multiple Serum / Solana ecosystem projects such as BonFida, Oxygen Protocol and MAPS, which all launched tokens in a short expanse of time.

Here’s the full thread from SBF shilling all of these in Dec 2020, comparing products like Maps to Paypal.

According to my sources at the time, much of Serum was operated by full-time FTX employees. Some Serum ecosystem projects were made to be seen as third-party projects but were, in fact, internally incubated/ operated. However, at the time, a lot of this was portrayed as FTX being hands-on supporters of an ecosystem it helped create, so most likely did not think much of it.

In fact, the prevailing narrative was laudable - a centralized exchange was investing heavily into technology that it believes will disrupt itself, and by doing so helped bootstrap a new ecosystem on Solana that offered radically different trade offs for users on Ethereum (i.e. higher throughput, lower fees, with more centralization).

As a DeFi geek, I was excited. I hosted a debate between SBF and Synthetix’s founder, Kain Warwick, on the podcast, eager to see intellectual disagreement between one of DeFi’s pioneers and who I thought at the time was someone who could bring something new to DeFi.

Despite my intellectual curiosity, we also passed on most of the Serum ecosystem due to the opportunistic valuations and the way the raises were conducted, which didn’t give us enough time to ask the questions we needed.

We did put in a small check into a project called Bonfida - which at the time had a live dashboard akin to Zapper, and has created a name registry for Solana-based addresses. After two reference checks with folks who have worked with the founder, and meeting the founder in person, we decided to write a small check as a hedge to us being wrong about Serum. On one hand, it seemed like a low-level enough bet to offer some broad based index exposure to Serum should it take off; on the other hand, the product was actually live - which was more than what you could say for most DeFi projects raising at the time.

Later, FTX would enable FIDA - Bonfida’s native token - as a collateral type on the exchange, which struck us as highly unusual given the illiquidity and nascency of the asset.

So why did FTX do this?

Alameda's Eroding Edge and Strategy Drift

First, some context. Assuming Alameda and FTX were much closer than they represented, something changed internally with Alameda/FTX around that time (winter 2020).

Namely, Alameda moved AWAY from delta-neutral strategies and began to assume directional risks in crypto. A detailed, unverified subjective account here for you to bookmark:

One hallmark of delta-neutral traders (i.e. takes no directional risk in a market; all positions are offset by a bet in the opposite direction) is their penchant for leverage. If your strategy has a 2.0+ Sharpe and you can scale your returns without proportionally scaling your risk - your logical choice is to lever up and bet as much as possible!

However, once the trader goes directional (i.e. takes a view on where the market goes), levering up also increases your risk. Many delta-neutral traders, when they wade into directional strategies, can’t seem to shake their appetite for leverage despite mathematically understanding the increased risk they can incur.

So how did the Serum assets fit in the story?

They were likely used as collateral to enable the aforementioned leverage. All traded at thin circulations, so it was easy to manipulate an artificial price for them and use them to pad Alameda’s balance sheet.

If you’re unclear on how this works, here’s a primer on the concept of FDV and how it can be manipulative. I received a lot of flack from industry peers for posting this in 2020 (“FDV is a meme”) as it got in the way of VCs shilling their massively overvalued assets at deceptively low market capitalizations, but you see now what it mattered.

To give an example, let's say Alameda funds a semi-incubated project at a $10M "fully diluted valuation" (price of token * total number of tokens ever to be issued) with $2M.

FTX then lists the token on its exchange but only releases 1% of the total tokens to market.

As markets are thin, Alameda can prop up prices using a few million dollars to create a "fake" fully diluted valuation of say $1B - suddenly, $2M is $200M on *paper*. This is an open secret for what industry insiders call "Sam coins".

Note the circulating supply across them (hint: they are all very low, relative to the fully diluted valuation!)":

By doing this, Alameda creates the illusion of a large + diversified balance sheet, which it could then borrow against to fund directional bets. FTX also lists swaps contracts for "Sam coins", which means Alameda can short their own investments/incubations to lock in profits on unvested tokens.

Insiders who questioned the legitimacy of these schemes seemed to be personally bullied and threatened by SBF into silence. One of many accounts from ex-employees or those that worked with/under SBF reached out to me to provide the following account:

All in all, this circus created hundreds of millions for Alameda/ FTX in equity value, based on a very illiquid market, as its leaked balance sheet showed.

The punchline?

All of this was dwarfed by its $FTT holdings…

Planting the Seeds for Alameda’s Undoing: FTT

Some of the Serum coins and FTT itself were pledged on FTX- the only exchange to allow such assets to be used - as collateral. Some of it was likely used to borrow from credit desks.

This is likely how Alameda/FTX incurred the multi-billion dollar hole:

Alameda pledged illiquid collateral to borrow money to finance bets, which got margin called as markets went down this year, leading to the theft of FTX user funds to put out fires.

This means that liquid reserves on FTX were likely lower in amount than user deposits. Chances are this hole was considered to be manageable given enough time as more of FTX/Alameda's illiquid assets get vested over the years.

That is, until the founder of Binance, CZ induced bank run on FTX (more later).

Subsequently, SBF would attribute the multi-billion hole to an accounting oversight, but in my experience attributing to ignorance what can be easily explained by malice - particularly in competent people - is naive.

We will return to FTT later.

Keeping the FTX Ponzi Going: SBF’s Confidence Game

As all of this was brewing in the background, SBF was aggressively pushing for mainstream legitimacy and establishing a regulatory moat - the two things that would ensure the equity value of FTX and $FTT, which they likely used to finance leveraged bets do not collapse.

By making more profits, SBF could acquire more FTT, which allowed them to obtain more leverage…you get the idea.

To do this, FTX increased their marketing.

The most dramatic examples: a $135M deal to rename the Miami Heats Stadium, being the second biggest donor to Joe Biden, and a failed attempt to join Elon Musk’s Twitter bid (happened post recent raise).

The subsequent rounds of fundraises that pushed FTX's valuation to $32B (Jan 2022), bringing in Paradigm, Sequioa, Tom Brady and Singapore’s state fund Temasek were widely documented.

The point is FTX was quickly capturing mainstream mindshare, bolstered by retail-facing ads as well.

Amidst the growth in retail mindshare and aggressive capital raise, SBF was making a push in policy too. It is important to note that SBF's parents - Joseph Bankman and Barbara Fried - are both professors at Stanford Law School

The above is important as the family is known to have strong ties to the Democrats in the US. A more detailed thread on SBF's familial relationships and *deep* political ties can be found here - you can bookmark and read it later. It bordered a bit on conspiracy theory, so I will not recount it here.

The way this is relevant is SBF was exercising his considerable political muscles to establish a regulatory moat for FTX. In Oct 2022, FTX proposed a standard for regulation that widely favored FTX over any DeFi competitors.

This was widely seen as a “kicking down the ladder” move - wherein after Alameda famously profited by opportunistically “farming” DeFi tokens and dumping them on retails, they moved on to ban others from doing the same.

2022 Bear Market: The Cracks Appear

Amidst the noise, one seemingly inconsequential event took place in August of 2022.

Sam Trabucco, co-CEO of Alameda at the time, announced his stepping down from the firm in the depths of the crypto bear market. This did not raise much alarm at the time...but it should have.

A month later, FTX secured a $1.4B bid on Voyage Digital, a brokerage firm that went under due to the collapse of Three Arrows Capital earlier this year. Court documents show that Voyager has >100K creditors and billions in liabilities.

So assuming FTX already was facing financial woes at this time, why would they bid for Voyager when it itself is in a cash crunch?

This is pure conjecture - but the likely explanation is that FTX was likely bailing out entities with large FTT holdings to prevent forced selling, as much of its own leverage is backed against $FTT.

Not long after, as SBF sought to establish legitimacy in Washington, his and CZ’s commercial feud gives way to a Twitter spat. Below is a deleted tweet from SBF.

Shortly thereafter, CoinDesk released a concerning piece regarding Alameda's balance sheet, citing that a huge part of its $14.6B in assets are assets issued by the FTX team itself.

The sharks smell blood now.

FTX’s Bank Run and SBF’s Lies

On Nov 06 2022, CZ stated that in light of revelations regarding Alameda's balance sheet, Binance will liquidate the entirety of its whopping ~$584M in FTT.

In response, Caroline Ellison, sole remaining CEO of Alameda, cites that ~$10B worth of assets are not reflected by the balance sheet reveal, which is echoed by SBF. This added to fears that Alameda and FTX were more commingled than publicly perceived.

Caroline then makes a public offer to CZ to purchase all $FTT at $22, leading to speculation that perhaps Alameda had loans that would be liquidated if FTT traded under that price.

Markets started to react in panic.

As of Nov 07 2022, according to Nansen, ~$450M worth of stablecoins left FTX within 7 days - a bank run is set in motion. On Nov 08 2022, SBF assured the public that FTX is "heavily regulated" and GAAP audited, with $1B in excess cash.

This tweet has since been deleted by SBF as well.

At the time, FTX CEO Ryan Salame calls @cz_binance "the worst" in a now-deleted tweet, as multiple junior to senior employees attempt to allay public fears and stop the bleeding. Since then, some of them have been active in assisting creditors in getting a hold of recent developments at FTX - whether this is an attempt to genuinely be of service, or to distance themselves publicly to avoid suspicion - remains to be seen.

Based on internal chats shared with me, SBF, who was fully aware of the situation at the time, seems to have kept his employees in the dark and asked them to publicly commit fraud.

Shortly after, SBF publicly claimed that FTX DOES NOT INVEST CLIENT ASSETS, EVEN IN TREASURIES, and that it has enough to cover all withdrawals.

This tweet has since been deleted.

Withdrawals from the exchange were soon frozen on Nov 08 2022, with no further communication from FTX.

On Nov 09, SBF announced a potential deal with Binance and made another fraudulent assurance that assets were 1:1 backed.

While withdrawals were frozen, Alameda was still able to siphon funds off of the exchange.

When asked why, Caroline claimed this was the FTX US exchange, implying that only the FTX International entity was facing liquidity issues. On Nov 10th, CZ announced that chances for a potential bail-out deal are off as suspicions arise that the hole was too big to fill.

In an internal note on Nov 9th, CZ stated that Binance did not "master plan" the demise of its competitor. I find this credible as well as the disorderly collapse of FTX will likely decimate crypto markets for years to come, which is against Binance’s interest. However, it is also likely that CZ saw no other alternative to remove a competitor without market disruption and opted to engineer a bank run sooner rather than later to prevent further contagion.

Shortly after, withdrawals seemed to have resumed on FTX. Later, FTX would claim that this is part of its compliance with regulations in Bahamas, where FTX's HQ is based but Bahamian regulators would soon debunk this in an official statement.

Below is a DM leaked to me, where SBF seemingly instructed one of his employees to once again commit fraud publicly.

But if not Bahamians locals, who was cashing out millions at a time?

FTX Burning Down, but Employees Cashing Out?

From a primary source I can confirm that at least one employee - who is neither Bahamian nor based in Bahamas - was able to successfully withdraw assets.

Speculation began to arise that insiders were cashing out, and commingling their withdrawals with actual Bahamaian users.

Soon, users began to find ways to exploit the loophole, with at least one prominent crypto trader supposedly purchasing Bahamian KYC'd accounts to launder assets out. Multiple secondary accounts about employees bypassing KYC mechanisms using internal contacts were also relayed to me, but I will leave it to the journalists to get to the bottom of this.

On Nov 11 2022, Founder of Tron Justin Sun announced a credit facility to allow part of FTX's users to withdraw capital via assets associated with the Tron network. This led to a massive premium in $TRX price on FTX.

For some inexplicable reason, SBF never paused trading either for FTX - leading to alleged washtrading on multiple perp pairs, whereby a user would intentionally lose against an account that was able to withdraw in order to cash out.

FTX + SBF also never responded to questions regarding Bahamas withdrawals, and whether insiders cashed out. But the comms blackout was conveniently timed right before a public announcement for FTX's bankruptcy on Nov 11, 2022

FTX Files for Bankruptcy…Then Gets Hacked

After the bankruptcy announcement, withdrawals were finally paused; however, hundreds of millions began to be siphoned from FTX. General Counsel Ryne Miller claimed that FTX was moving its own assets to cold storage.

This was likely not the entire truth as seasoned onchain sleuth ZachXBT revealed a potential hack has likely occurred. Miller then responded with an official statement regarding cooperation with law enforcement to secure stolen assets.

The fact that SBF and Ryan Salame did not have tighter opsec and lock down or pause trading and withdrawals when multiple employees were claiming they were lied to and clearly disgruntled was a monumental failure in management. After a brief period of silence, @SBF_FTX began to taunt the public by tweeting cryptic, one letter tweets on Nov 14, 2022.

Crypto investor Erica Wall revealed that SBF was likely using the tweets to fool bots that are designed to detect tweets being deleted - this is currently unproven and unlikely.

Details regarding the potential hack are still unfolding.

FTX Seemingly in Damage Control

Earlier on Nov 15, Reporter for New York Times David Yaffe Bellany who has previously co-written a hit piece on rival exchange Kraken, published a piece on SBF. This was widely considered to be a puff piece.

This was quickly followed by a piece from the Washington Post, which bizarrely focused on how the collapse of FTX prevented SBF’s pandemic prevention efforts….rather than the billions of dollars in stolen money and outright financial fraud with public documentation (?)

This led to widespread suspicion that FTX has a degree of influence over certain publications, which may very well be founded in SBF’s political ties.

FTX: The Aftermath

Most recently, news regarding loopholes in FTX's backend that allowed SBF to launder user funds seem to have surfaced but currently unproven.

According to at least 3 primary sources from FTX, only 4-5 senior executives likely knew the full extent of FTX's woes until the very end.

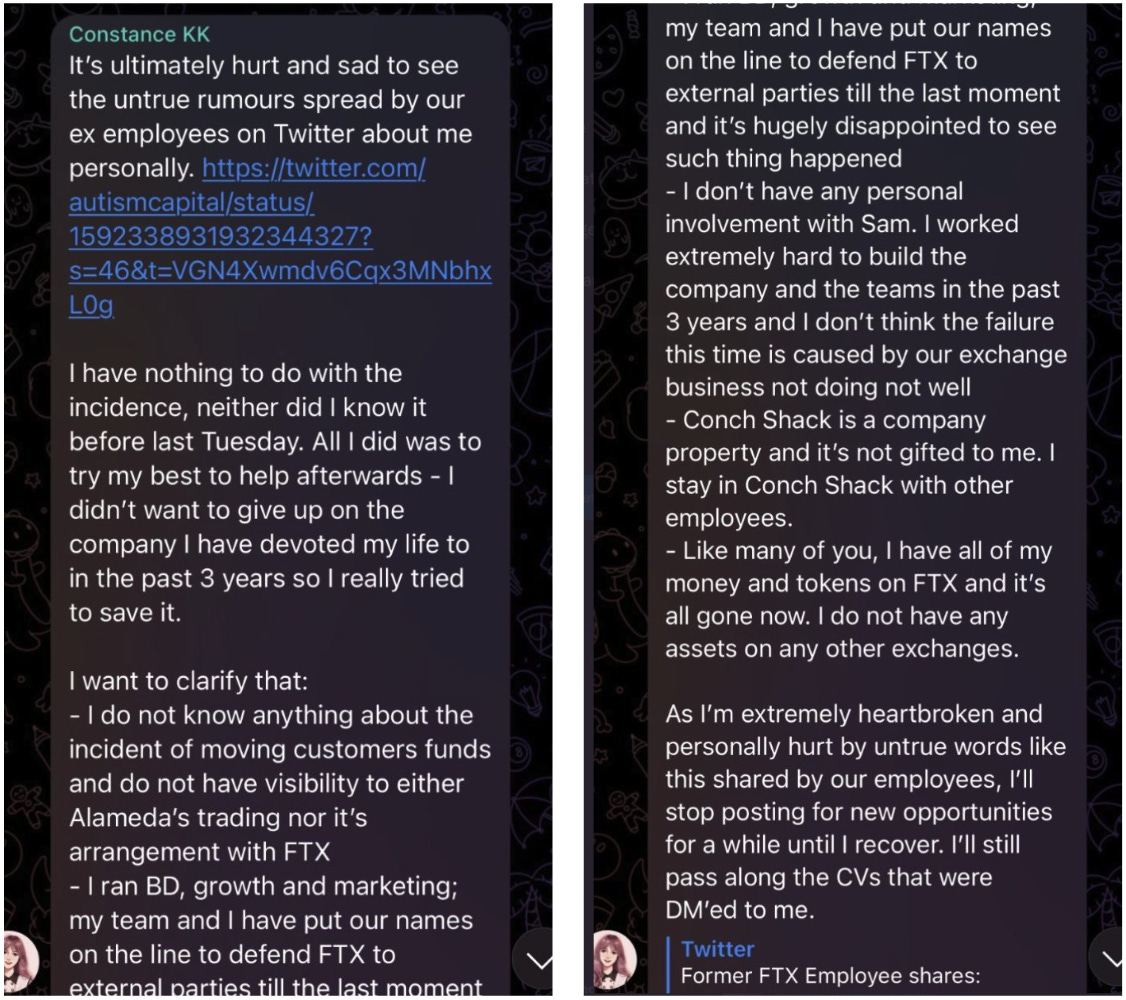

I am not privy to how legitimate these claims are and there may be a chance that none, all, or people beyond the list of people are complicit, but for public interest the names shared with me were: SBF, Caroline Ellison, Gary Wang, Ramnik Arora, Constance Wang, Nishad Singh.

In another leaked screenshot, Constance allegedly has come out to deny her involvement.

There are a lot more interesting facts - such as Caroline’s blog, SBF’s supposed stimulant addiction, alleged orgies in the FTX office - which I don't think are that relevant for those who seek to understand what happened.

I will leave the tabloids for New York Times.

This will (hopefully) be the last development, short of prosecution and paying out of creditors, for the FTX saga.

Edit: since the publishing of this post, a “journalist” has shared a letter supposedly sent by SBF to his employees and attempted to downplay the publicly documented fraud as an issue in mismanagement of assets. We found out soon that SBF is an early investor in the publication; this was not properly disclosed.

I've also recorded an abridged, 20-min version of this on my podcast The Blockcrunch, which you can find on Spotify, Apple and YouTube

The Blockcrunch Podcast (“Blockcrunch”) is an educational resource intended for informational purposes only. Blockcrunch produces a weekly podcast and newsletter that routinely covers projects in Web 3 and may discuss assets that the host or its guests have financial exposure to. Views held by Blockcrunch’s guests are their own. None of Blockcrunch, its registered entity or any of its affiliated personnel are licensed to provide any type of financial advice, and nothing on Blockcrunch’s podcast, newsletter, website and social media should be construed as financial advice. Blockcrunch also receives compensation from its sponsor; sponsorship messages do not constitute financial advice or endorsement.