What You're Missing About dYdX v4: A 30-Page Deep Dive

Tokenomics, Unlock, and Comparisons to other Perp DEXs

Blockcrunch VIP is a premium research newsletter on the most important crypto projects and trends, prepared by top crypto analysts twice a month. Subscribe to Blockcrunch VIP to receive in-depth project analysis from our research team - all for the price of a coffee ☕ a day.

One of the biggest activities in cryptocurrency is trading and speculation, and although centralized exchanges (CEXs) are where most of the trading takes place, decentralized exchanges (DEXs) continue to grow in popularity as they do not require a central intermediary to facilitate trades.

DEXs to CEX spot trading volume has continued to grow over time and now makes up about 10-20% of CEX volume. As DEXs continues to improve in capital efficiency, UIUX, and security, the spot volume on DEX should continue to grow against CEX.

In traditional finance, financial markets tend to evolve from spot-driven to derivative-driven. A derivative is a financial contract which price or value is derived from an underlying asset. The most common types of derivatives in crypto are perpetuals (which are a type of futures) and options. According to most estimates, derivatives trading volumes tend to be higher than cash trading volumes. This is due to derivatives providing additional utility, such as leverage and hedging.

Evolution of Assets: Spot → Derivatives

Thus as crypto grows and becomes more financialized, it is expected to follow the same trajectory as traditional finance, where derivatives volume outgrows spot volume. Crypto derivatives now dominate the market with 74.8% share of crypto's total trading volume.

Source: CoinGecko

However, this derivative volume is made up of over 98% from CEXs and less than 2% from DEXs. Why is this figure so low and stagnant for so long?

In order for perp DEXs to outperform CEXs, they must outperform in three key areas: user experience, security, and governance. One of the largest perp DEX, dYdX, which makes over a billion in volume a day, has recently improved these key aspects with their v4 migration.

However this migration also coincided with a recent token unlock which has increased their circulating supply by about 80% overnight and increased inflation henceforth, causing investors to be cautious. Will the improvements in dYdX v4 be sufficient in boosting investor confidence versus the new supply inflation?

In this week’s report, we aim to provide an in-depth analysis of dYdX, its new tokenomics, and how it compares with others. Join us as we unfold the layers of these significant developments in the world of perp DEXs.

What is dYdX?

dYdX, founded in 2017 is a decentralized perpetual exchange and raised four rounds and was invested by A16Z, Coinbase, and Paradigm.

A Brief History

It is important to know a brief history of dYdX to understand their philosophy.

dYdX started on Ethereum in 2017 as a perp DEX with lending and margin, and in 2020 it was making up 50% of the trading volume while subsidizing gas fees. However, as DeFi and Uniswap became popular, gas fees increased, and dYdX was paying $100 for each trade and was not able to compete with the unlimited amounts of markets that Uniswap had.

Thus in 2021, dYdX migrated from Ethereum to Starkware to resolve the TPS and gas fee issues. This migration was known as dYdX v3 which still remains as the #1 perp DEX in terms of volume as of this writing.

Why dYdX v4 and Cosmos?

After FTX collapse, dYdX committed to becoming a fully decentralized protocol. As dYdX v3 still relied on a centralized orderbook and matching engine, they decided to move on to their own app chain, branding it as dYdX v4.

Version 4 of dYdX is a Layer1 chain based on the Cosmos SDK and will completely decentralise its matching engine and orderbook. The protocol won't have any more central points of failure or control because all of its aspects will be totally under the governance of the community.

Core improvements include:

Throughput: Currently ~500 orders are processed per second using dYdX's off-chain orderbook and ofinfrastructure, and v4 would enable even greater order capacity of ~2000 orders per second.

Finality: Traders will have immediate finality on the outcome of their trades with the off-chain matching engine.

Fairness: Network administrators and frontrunners shouldn't be able to profit from regular trading activities, and placing orders requires no gas fee, only charging upon completion.

Value Accrual: $DYDX token stakers now receive trading fees in the form of dYdx and USDC.

Other improvements include new trading products like spot, margin, and synthetic goods; enhanced collateral and margining; improvements to trading and market structure; and seamless addition of new markets.

There are several reasons why dYdX selected Cosmos compared to other rollups:

Customizability: Cosmos SDK allows for better performance, scalability, composability and governance.

Governance: Cosmos governance module facilitates decentralized governance which lowers the risk of regulatory scrutiny and allows it to reach more users.

Native USDC: Noble is bringing native USDC to Cosmos which should boost dYdX's liquidity and safety.

MEV-resistant: Cosmos's ABCI++ vote extensions and regular batch auctions integration help mitigate the impact of transaction ordering and MEV.

How does dYdX Chain work in dYdX v4?

The dYdX Chain will function similar to those of other Cosmos app chains.

There are 60 validators that can join the active set at genesis. This implies that a validator has to rank in the top 60 stake-weighted validators in order to contribute to consensus and get rewards for delegates. Slashing penalties are set to zero at launch, and there is a 30-day stake unbonding time. These settings are subject to change at any moment by governance; current parameters can be verified directly.

In order to receive staking incentives, token holders, also known as delegates, can stake / delegate their tokens to as many validators as they choose, which will lock the tokens until it is unbonded.

Exploring dYdX Tokenomics

Now let’s explore the numbers behind dYdX tokenomics and how it fares with others.

dYdX Value Accrual

In terms of tokenomics, perp DEX tokens are some of the strongest tokens in the cryptocurrency space as they usually offer a clear value accrual combined with sustainable token utility.

In dYdX v3, all trading fees flows to dYdX Trading, Inc. The DYDX token has little use beyond governance and staking to earn discounts on fees and other platform perks.

In dYdX v4, trading fees will be allocated proportionately to DYDX token stakers. Trading fees will be predominantly in USDC but also includes DYDX tokens used for gas. DYDX token will also be used to secure the dYdX chain by validators.

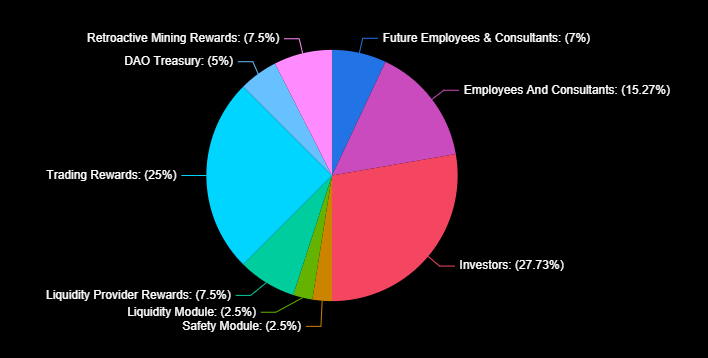

dYdX Allocations and Unlock

Let’s talk about the elephant in the room, which is dYdX’s huge unlock to insiders. It was previously delayed from January 2023 to December 2023, partially due to concerns about what it would do to the token’s price during a bear market.

How big is the allocation to insiders?

The allocation for dYdX token consists of 50% insiders (investors, employees, and consultants), 45% rewards, and 5% to the DAO. The 50% component has started being vested as of December 1, 2023.

About 34% have been unlocked including the most recent unlock, and another 66% that will be unlocked from now till August 2026.

Starting with about 36 million dYdX tokens on 1st Jan 2024, a decreasing amount of dYdX tokens will be released to the Team and Investors. At dYdX’s current price of $2.92, this translates to an average daily inflation of about $3.5 million.

If you include the Community and Rewards Treasury, which is roughly an additional 60 million tokens on 1st January 2024, and 5 million tokens per month onwards, the average daily inflation in 2024 will be 826,000 DYDX tokens per day. At the current current price of $2.92, this is roughly $2.4 million worth of tokens daily.

However, community rewards are not immediately given out. At the moment, a proposal has been passed to distribute about 9 million DYDX tokens (about $26 million worth) from the Community Treasury as part of their 6-month trading rewards program. This is about 50,0000 tokens a day or around $146,000 a day, however they are capped at the dollar equivalent of the total trading fees generated by the protocol for that block. This is to prevent the protocol from over-incentivizing trading activity with token inflation.

Source: dYdX

Now that dYdX v4 is live, will its fees and value accrual be sufficient to cover this potential selling pressure?

dYdX Unlocks vs Value Accrual in 2024

As mentioned above, in the most bearish scenario which assumes all tokens get sold, the average unlock value per day next year with $DYDX at $2.92 is $2.4 million. However, that is not realistic.

Here are the % distribution as well as a few scenarios to consider:

The base case assumes 32% of the community treasury is used and sold which is about 18 millon tokens. This number is derived by annualizing the ongoing 6-months trading incentives of 9 million DYDX tokens. Moving on, we assume investors sell 40% of their tokens. In comparison, employees sell 30% of the tokens, and 10% of the tokens are sold for future employees (which is already $8.8 million in annual salary). All trading rewards and liquidity provider rewards are completely sold. This results in a potential daily sell pressure of $838k.

Now let’s take a look at the daily fee of DYDX. According to DeFiLlama, the average daily fee in the past 30 days is about $222k.

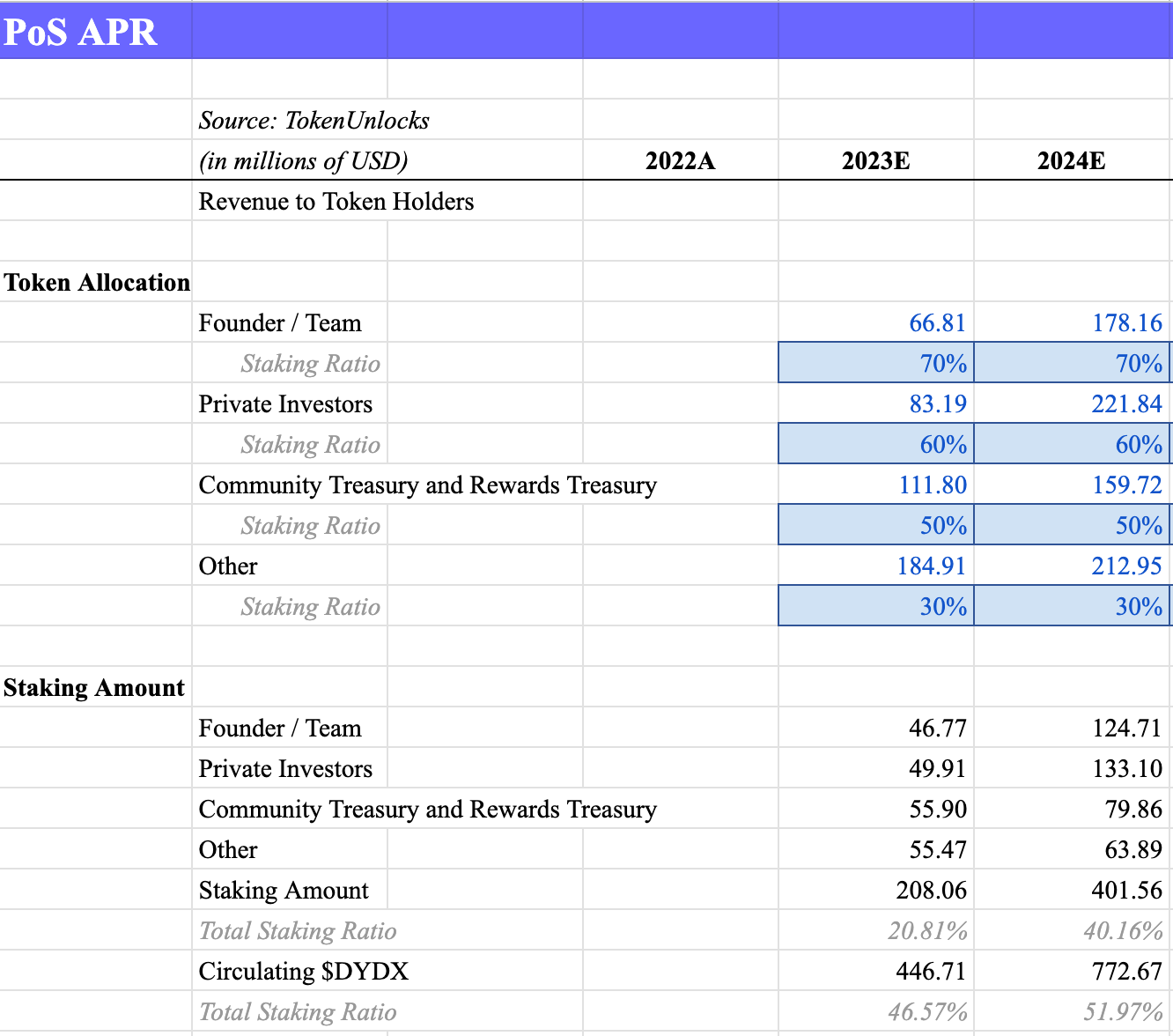

Assuming everyone staked their DYDX tokens, dYdX needs to increase the fees generated by about 4x for dYdX stakers to ‘break even’. However, the staking ratio will realistically not be 100%.

The current amount of bonded dYdX tokens is now 5% according to Mintscan. Assuming this ratio increases to 30% which is closer to other PoS chains, and the rest of the tokens circulated that were not sold gets staked, the total staking ratio will be about 50%. This means that the fees generated only need to be doubled to be higher than the inflation in the base case.

Estimating dYdX Staking APR in 2024

The staking APR is calculated by taking the total value of staked dYdX divided by the fees received.

The current perp volume is about 28 trillion annualized for 2023. Assuming this increases in 2024 to 50 trillion, and dYdX perp market share remains at 37%, it’ll generate about $258 million in fees to stakers.

The amount of circulating dYdX will be about 750 million in 2024, and if dYdX price remains at $2.92, with a staking ratio of about 50%, the total valued staked will be about $1.1 billion, resulting in a staking APR of about 22% from real yield.

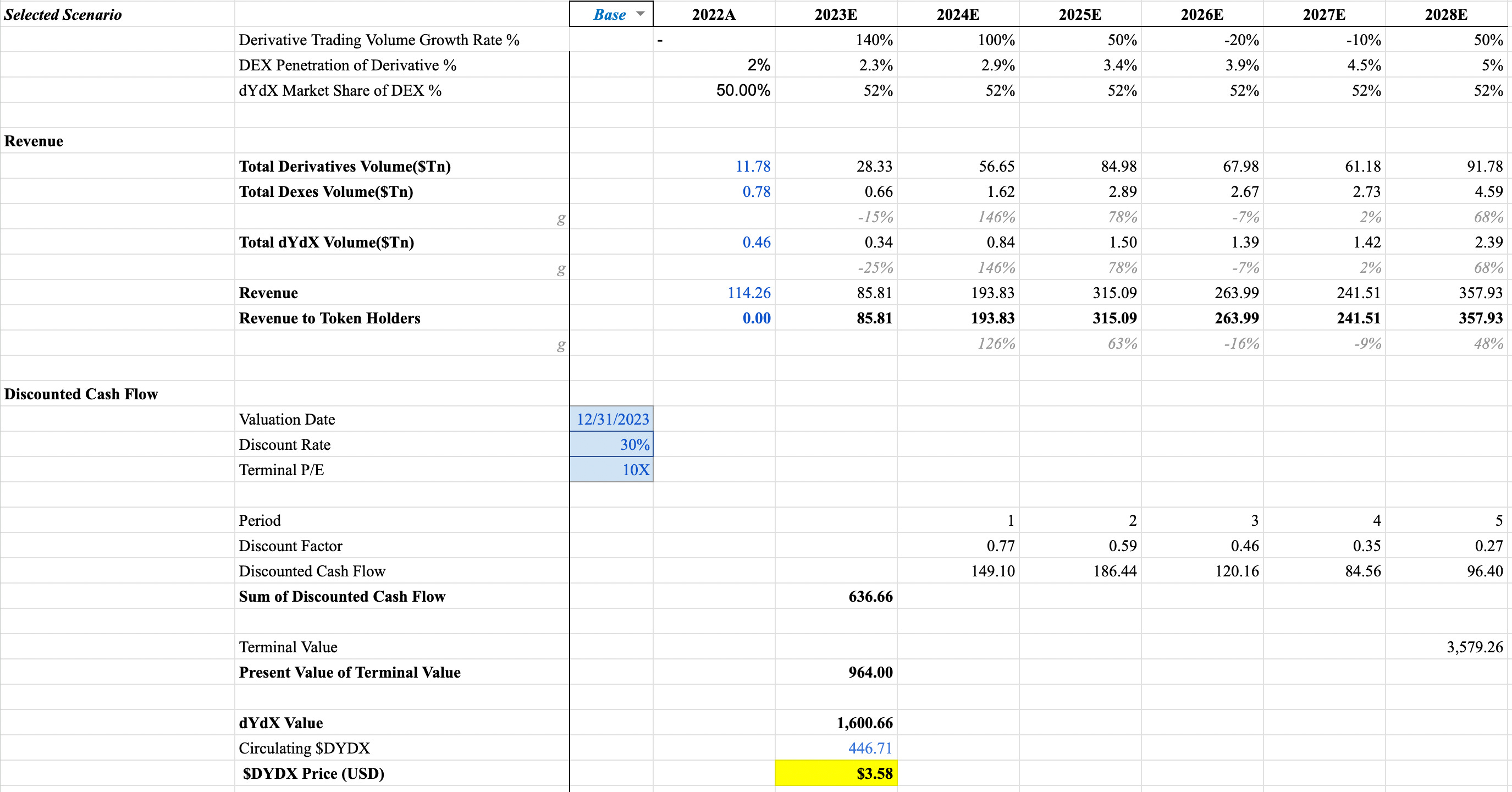

dYdX Discounted Cash Flow Valuation

Disclaimer: The valuations below are purely hypothetical and based on assumptions, and are not an indication of our view on price.

As dYdX is a revenue-generating protocol that provide returns to stakers, we can project the price of dYdX using Discounted Cash Flow (DCF) models.

Assumptions:

For simplicity, we will use a discount rate of 30%, a high figure as perp DEXs is a high-growth and high-risk sector. (The discount rate was calculated using the basis trade rate of BTC for the risk-free rate which is 9.53% and using BTC as the market benchmark, and it is calculated using CAPM. However, due to the recent market pump, this approach would have created an unrealistic discount rate of 75%.)

The Terminal P/E will be 10x as the current P/E of dYdX is 30x and other prominent DEX protocols are around 10x or lower.

The estimated trading fee remains at 0.025% as it is already relatively low and there will likely continue to be trading rewards and rebates as well.

Base Case

In our base case, we will assume that dYdX hits its previous all-time high volume in the next bull market which we assume in 2024 due to the Bitcoin ETF approval and is proceeded by the Bitcoin halving rally in 2025.

We will also assume that the derivative volume continues to grow in 2024 and 2025 by 100% and 50% respectively, hitting shy of 100 trillion volume, before falling as crypto enters a bear market in 2026, and going up again in 2028 due to the next BTC halving.

We also assume that dYdX market share remains the same at roughly 50% and that perp DEX penetration grows from the current 2% to 5% by the end of 2028.

This projects a dYdX price of $3.58 by 31 December 2023, and a market cap of $1.6 billion.

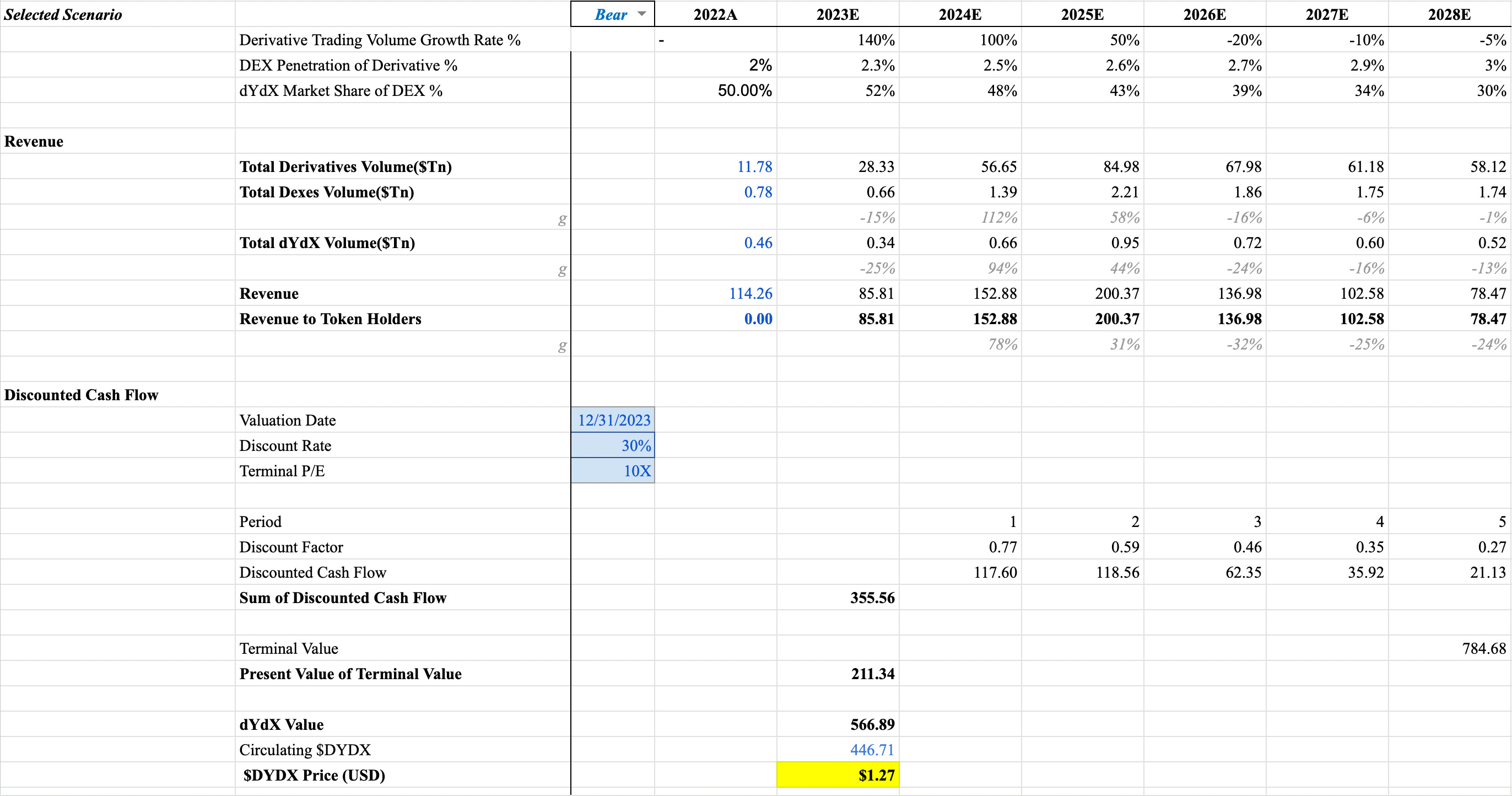

Bear Case

In our bear case, we will assume that the derivative volume grows similarly to the base case, however, we assume that dYdX market share drops to 30% as it loses out to competitors, and that perp DEX penetration grows from the current 2% to only 3% by the end of 2028.

This projects a dYdX price of $1.27 by 31 December 2023, and a market cap of $566 million.

Bull Case

In our bull case, we will assume that the derivative volume grow much more aggressively as institutions enter in bulk after the Bitcoin ETF approval and achieves 100 trillion in derivaive volume in 2025.

We also assume that dYdX market share grows to 60% as it gains marketshare from institutions, and that perp DEX penetration grows from the current 2% to 10% by the end of 2028.

This projects a dYdX price of $11.42 by 31 December 2023, and a market cap of $5.1 billion.

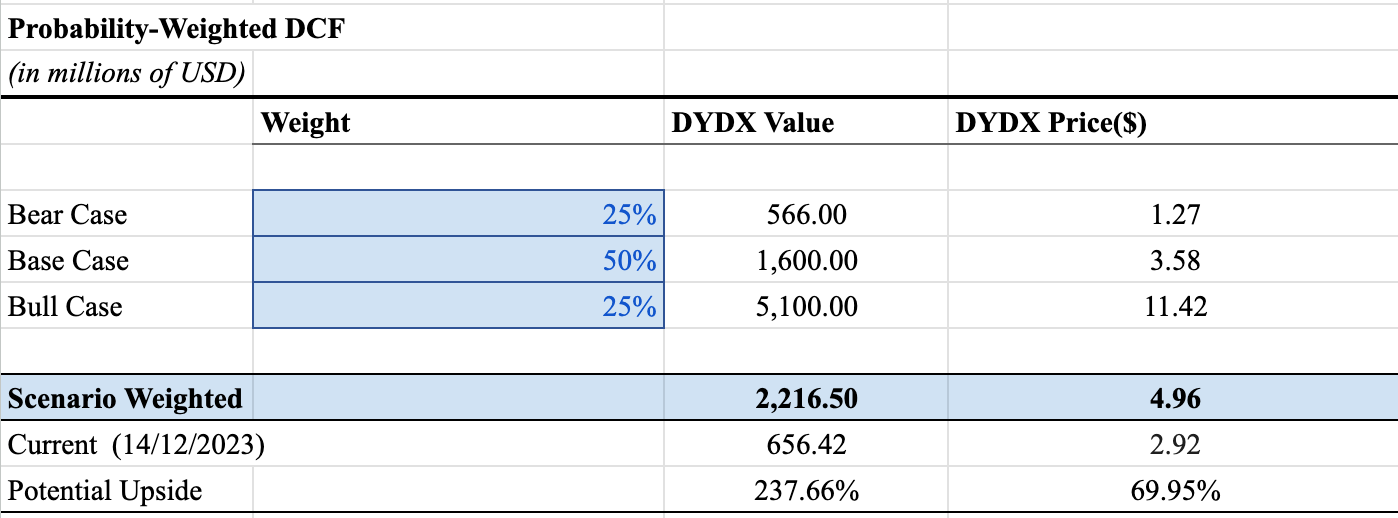

Probability-Weighted DCF

Based on the above scenarios, and giving a 25% probability to the bear and bull case with a 50% probability to the base case, the price of dYdX would be around $5 with a $2.2 billion market cap, which is about a 70% increase from the current price. If the bear-case scenario were to be realized, the price could go to $1.27 which is about 56% down from here. This provides a risk-to-reward ratio of 1.25 from the current price.

Competitive Analysis

Let’s compare dYdX with some of the established and newer perp DEXs.

Methodology for fees: When it’s not taken from DeFiLlama, it’s calculated by adding both the maker fees and taker fees and multiplying by the volume.

Positive takeaways for dYdX:

Largest verified volume and thus have the highest fees charged

One of the highest trader usage

dYdX has a healthy P/S ratio between 3 to 10

Negative takeaways for dYdX:

One of the most expensive in terms of FDV

It has one of the lowest float, meaning there’s probably more sell pressure

Interesting observations:

Despite dYdX having the most volume, GMX made the most amount of fees due to the fees they charged.

Hyperliquid has the highest amount of traders, this could be due to having the most perp markets (90+) on top of an airdrop and a 1 second deposit time from Arbitrum.

Comparative Projections

Let’s see how dYdX compares with other perp DEXs as we extrapolate volume, revenue, and P/S ratio.

Volume Projection

The existing annualized perp volume is about 30 trillion. With the bull market incoming, the volume is expected to grow rapidly, and we could even see 100 trillion annual perp volume. The current perp DEX volume compared to total perp volume is 2%, and if this figure increases by just 1% to 3%, it brings several hundreds of billion of volume to perp DEXs.

Revenue Projection

The revenue is generated by taking the volume multiplied by the average fee %, which is calculated by taking the volume divided by the total fees reported.

These figures alone don’t mean much, so let’s move on to P/S ratio.

Fully Diluted P/S Ratio Projection

In the next bull run, the projected annual perp volume is expected to grow to at least 50 trillion, and perp DEX volume penetration is expected to grow to 3%, producing very healthy full diluted P/S ratio for dYdX at 7.59, while GMX and RabbitX come in lower at 0.79 and 1.62 respectively.

What does this mean for the price of these tokens?

Price Projection

Assuming their fully diluted P/S ratio remains the same as today while the market grows, these are the possible prices of dYdX and other tokens. With the current price of $2.92, if the market grows to 50 trillion perp volume next year and 3% perp dex penetration, dYdX can grow by another 35% to $3.95 while maintaining it’s P/S ratio.

Perp DEX Innovations

Perp DEXs have come a long way since the previous bull market. GMX popularized the peer-to-pool model and oracle-based DEX, allowing anyone to be a market maker and counter party to traders.

Hyperliquid provides CEX-like trading experience with the most amount of perp markets, subsecond block times, and signless transactions.

Vertex brings hybrid liquidity (AMM + Order book) and cross-margin which allow users to trade with other collateral as margin, increasing their capital efficiency.

Aevo is on its own optimism rollup chain and just introduced yield-bearing collateral, allowing users to earn short-term US Treasury Bills while trading, allowing their liquidation price to move further away as they hold the position (excluding funding rate).

SNX is introducing a buyback and burn mechanism to be deflationary as well as launching their own CEX called Infinex to compete with other CEXs.

dYdX moved to its own app chain with amazing features and is finally bringing revenue distribution to stakers.

Other perp DEXs on Cosmos include Demex and Levana with their own unique features such as replicated liquidity and no insolvency risk while still teasing airdrops.

Are These Innovations Good Enough?

As mentioned in the beginning of this article, there is a huge discrepancy where 98% of perp volumes happens on a CEX. Apart from more marketing, for a DEX to take market share from a CEX they have to out perform in these areas:

User experience

Governance

Security

User Experience:

This is how well the product matches traders’ desires and it’s arguably the most important element in determining how much traction a perp DEX gets.

This includes areas such as liquidity, performance, fees, onboarding process, accessibility via a native mobile app, ease of use by having push notifications, having the most number of markets to trade, etc.

Speaking of fees, most perp DEXs offer trading incentives that make their net fees on par or even cheaper than CEXs. During a bull market such a strategy would be critical in persuading traders to move from CEXs to DEXs.

Although dYdX have improved their technology and trading performance, it still lacks a large variety of markets to trade with with only 38 compared to Binance’s 296 markets. They also do not list any markets not already available on CEXs, thus there is little reason for dYdX traders to move over.

Additionally, dYdX v4 requires bridging into the platform, which takes about 20 minutes when bridging from an EVM network. Although this can be faster than centralized exchanges which require KYC that can take hours or even days to process, other perp DEXs have a faster onboarding time.

Hyperliquid, a relatively new DEX, has more traders than dYdX. This can partially be attributed to their aggressive listing strategy where they list new markets, even special markets such as pre-launch perps that cannot be found on CEXs. If the only place to trade certain markets are on Hyperliquid, it is almost guaranteed that traders will move over from other perp DEXs and CEXs.

Governance:

This is the major area where decentralized exchanges (DEXs) diverge from centralized exchanges (CEXs).

Governance is being able to dictate how an organization is run, such as how much fees you as a token holder would get. In contrast, on CEXs like Coinbase or Binance, all governance and platform decisions are controlled solely by the private corporate owners of the exchange, without any input from community token holders or users. Although dividends and fees are given back to shareholders / token holders either directly or indirectly, they do not have a say over it.

In dYdX v4, it has been fully decentralized, putting decision-making power back in the hands of token holders. On top of that, all fees go back to stakers which is a huge differentiator compared to CEXs. This also helps to create a sense of ownership and loyalty among users, achieving a network effect and positive flywheel. If traders can own a share of the revenue of the exchange they trade on, it can make them more willing to trade more, as well as bringing other traders onto the platform.

Although decentralized governance is more inclusive and transparent, it often makes it slower or harder to coordinate, allowing centralized exchanges the chance to be more productive and grow faster.

Security:

There’s no point in making a profit if you can’t secure it.

This is especially true since FTX’s collapse in November 2022. There was a strong narrative for perp DEXs right away and dYdX’s number of users increased by about 40%.

However, dYdX’s user growth was short-lived and the number of users quickly went back to normal the next month.

This shows that perp DEXs can take volume from CEXs only when there’s increased preference in security, but it is often fleeting as traders have higher priorities than the dangers of custodied trading.

Catalysts

The growth of dYdX's volume, as well as the overall derivative volume in the crypto market can be influenced by a variety of catalysts.

Mainstream Adoption after Bitcoin ETF Launch

A Bitcoin ETF approval would attract both retail and institutional investors who are more comfortable with traditional investment vehicles but interested in cryptocurrency exposure. As interest in Bitcoin grows, these investors may also explore derivative products for hedging or speculative purposes, potentially increasing the volume on platforms like dYdX.

It would also indirectly signal a shift in regulations, which will boost confidence in using crypto trading platforms, generating more volume which indirectly helps dYdX.

According to Juliano, about 80% of the volume comes from professionals who trade more consistently, helping their volume to maintain over a billion daily. With such strong track record of professionals, it would not be surprising that dYdX becomes the go-to platform for institutions.

Fed Interest Rate Falls

The Fed has indicated that U.S. interest rates will be cut in 2024 and 2025. This means that there will be a greater appetite for risk, and the demand for leveraged trading will grow, benefiting dYdX.

Product Improvements

dYdX spent over a year focusing on the migration to dYdX v4, during which they have not listed much new markets.

Now that it is done, they have mentioned that they will start focusing on listing new markets, having permissionless market listings, and trading tools to improve the trading experience.

It will be exciting to see what features they launch next to attract new traders.

Incentives and Revenue Share

A substantial reserve of funds remains available at the foundation for launching new liquidity mining initiatives, which have already started.

This can help dYdX continue to generate the highest volume in crypto, which in turn generate a lot of revenue to stakers which will help increase the sentiments about the dYdX token.

Risks

The upcoming unlocks are not the only concern that investors may have. Let’s explore some of the risks facing dYdX.

Regulatory Challenges:

Cryptocurrency exchanges require specialized compliance tools to adhere to OFAC and other U.S. regulatory standards. The recent sanctions on Tornado Cash and fines on Binance have increased concerns about regulatory adherence.

Additionally, when it comes to on-chain tracking for regulatory reasons, although Cosmos have their own analytics tool, it may not be as robust as established analytics firms like Chainalysis and TRM which have yet to integrate Cosmos.

Furthermore, although v4 is fully decentralized, dYdX's governance still appears to be influenced by its founder and major investors, leading to a more centralized decision-making process, together with the token revenue distribution model, dYdX can be seen as a security.

Lack of Adoption for v4:

dYdX v4 started trading on November 28, 2023, and as of this writing, December 13, dYdX has since generated about 3 billion of volume in about half a month, or an average of about 100 million volume a day.

This is only about 10-20% of the volume of dYdX v3 while still having trading rewards that subsidize up to 90% of trading fees.

This could be due to improvements in dYdX v4 is not perceived as being worth the hassle of moving funds over, especially since there isn’t a 1-click migration function.

If the dYdX team continues to develop dYdX v4 but user attention and traction does not improve, they could be losing current and future traders to other perp DEXs.

Security Concerns:

dYdX v3 uses Starknet which is an L2 Roll up that is secured by Ethereum. By moving to Cosmos, apart from spending on its own security infrastructure, users also have to trust dYdX chain’s validators which are not as well-known as Ethereum validators.

Additionally, dYdX v3 was attacked recently, and although user funds were not affected, dYdX insurance fund lost around $9 million which has affected dYdX credibility in terms of security.

Thesis

Perp DEXs capturing market share from CEXs is akin to a David vs. Goliath tale. It is more than just a battleground of features; for perp DEXs to win they have to either offer a giant leap in user experience or shift the priority of traders to security, both of which are possible but challenging for dYdX.

dYdX faces strong competition from new and established competitors, and their move to v4 have delayed their product roadmap.

If we expect the founders and investors to stake most of the supply that gets unlocked, which will generate an APR of more than 20%, dYdX just needs to double their volume to overcome the potential selling pressure, which is highly possible in an upcoming bull market.

Additionally, if the market continues to do well, based on the above analysis using the probability-weighted DCF scenario and a bullish outlook, the price of dYdX could go higher to between $4-$5.

Ultimately, the perp DEX space is highly competitive and dYdX could lose their #1 rank unless they catch up in innovation, execution, and marketing to compete with other perp DEXs as well as CEXs.

Disclaimer

The Blockcrunch Podcast (“Blockcrunch”) is an educational resource intended for informational purposes only. Blockcrunch produces a weekly podcast and newsletter that routinely covers projects in Web 3 and may discuss assets that the host or its guests have financial exposure to.

Some Blockcrunch VIP posts are written by contractors to Blockcrunch and posts reflect the contractors’ independent views, not Blockcrunch’s official stance. Blockcrunch requires contractors to disclose their financial exposure to projects they write about but is not able to fully guarantee no such conflicts of interest exist. Blockcrunch itself will not buy or sell assets it covers 72 hours prior to and subsequent to the publication of a piece; however, its directors, employees, contractors and affiliates may buy or sell assets prior to or subsequent to publication of any content and will make disclosures on a best effort basis.

Views held by Blockcrunch’s guests are their own. None of Blockcrunch, its registered entity or any of its affiliated personnel are licensed to provide any type of financial advice, and nothing on Blockcrunch’s podcast, newsletter, website and social media should be construed as financial advice. Blockcrunch also receives compensation from its sponsor; sponsorship messages do not constitute financial advice or endorsement.

For more detailed disclaimers, visit https://blockcrunch.substack.com/about