NFTfi: Understanding the NFT Lending Market

Evaluating the market leader in NFT Financialization

This is a free sample. Early annual plan Blockcrunch VIP subscribers receive weekly research briefs for the price of less than a coffee a week (<$2)

This week: NFTfi

Full interview with NFTfi: co-founder Stephen Young.

Executive Summary

Despite the mainstream awareness for NFT trading, brought about by Opensea, lending markets for NFTs only account for 6% of the entire NFT market and <0.25% of trading market activity.

Is lending for NFTs an inherently niche use case with mediocre growth prospects? Or is it the market expansionary catalyst DeFi has been waiting for?

To explore this, we examine NFTfi - the de facto market leader in NFT lending protocols today.

Below we share our thoughts on NFTfi, based on our pre-show research and interview with NFTfi co-founder Stephen Young.

Below we will cover:

What is NFTfi

How NFTfi’s P2P Model Works

NFTfi’s Team

Market Opportunity

Competitor Analysis

Catalysts

Thesis

FAQs

Tips

Resources

1. What is NFTfi

NFTfi is a peer-to-peer lending platform that allows NFT owners to borrow wETH or DAI using their NFTs as collateral, and lenders to earn interests by servicing these loans.

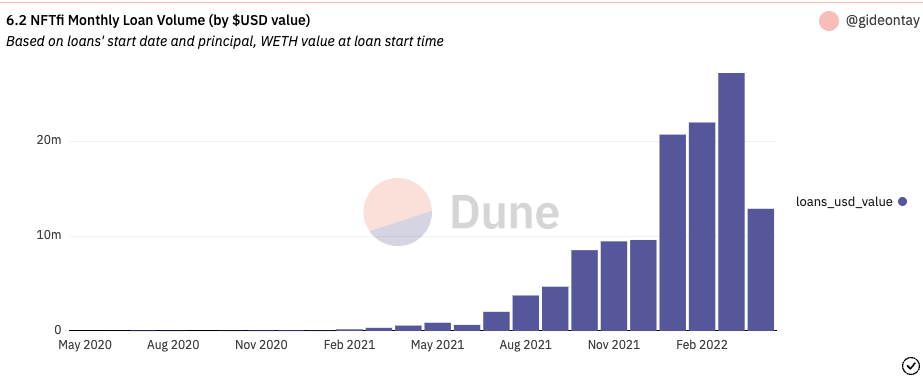

Since going live in May 2020, NFTfi has facilitated approximately $123 million in over 7,000 loans, and is currently the leading NFT-loan protocol by volume.

Typical loan durations are 7, 14,30 to 90 days, with short term loans requiring higher APRs up to 1,000% (effective 2-3% a day for a 10 day loan), whereas longer duration loans average around 90%. Default rate by loan amount is low (sitting at 6.34% according to Dune Analytics).

Some popular collateral types are as follows:

Wrapped Crypto Punks account for 28,530,494 DAI, or 75% of DAI loans and 29% of total loans.

Bored Ape Yacht Club NFTs account for 6942.98 wETH and 3,382,307 DAI in loan volumes, roughly 23% of total loans.

The single largest wETH loan today is 265.41 wETH (roughly $740K at market price), collateralized by The Eternal Pump #14

The single largest DAI loan today is 1,432,012 DAI, collateralized by Autoglyph #488

2. How NFTfi works

In NFTfi’s P2P model, the borrower lists her NFT to be used as loan collateral and she can choose to specify the loan amount, duration and interest rate.

The lender can either accept the terms as is or choose to counter-offer for the borrower to accept. Once there’s an acceptance of offer from either party, the loan is executed and NFT is sent to an escrow smart contract.

Unlike fungible tokens, it may not be possible to buy back a unique NFT once it is sold. For this reason, the NFTfi team decided to do away with the auto-liquidations that DeFi users have grown accustomed to in times of market volatility. Only when a borrower fails to repay loan + interest and expiration date has passed will a liquidation be triggered.

When this happens, the borrower loses her claim on the NFT collateral, and the NFT is transferred to the lender.

In our view, lenders’ risks are harder to predict than borrowers as they must factor in the risk of capital loss from “voluntary” defaults - i.e borrower forgoes her claim on the NFT and voluntarily defaults when the value of NFT is less than loan amount. This might be the reason why we see sophisticated whales (plus DAOs) making up a healthy percentage of loan underwriting on the lending side.

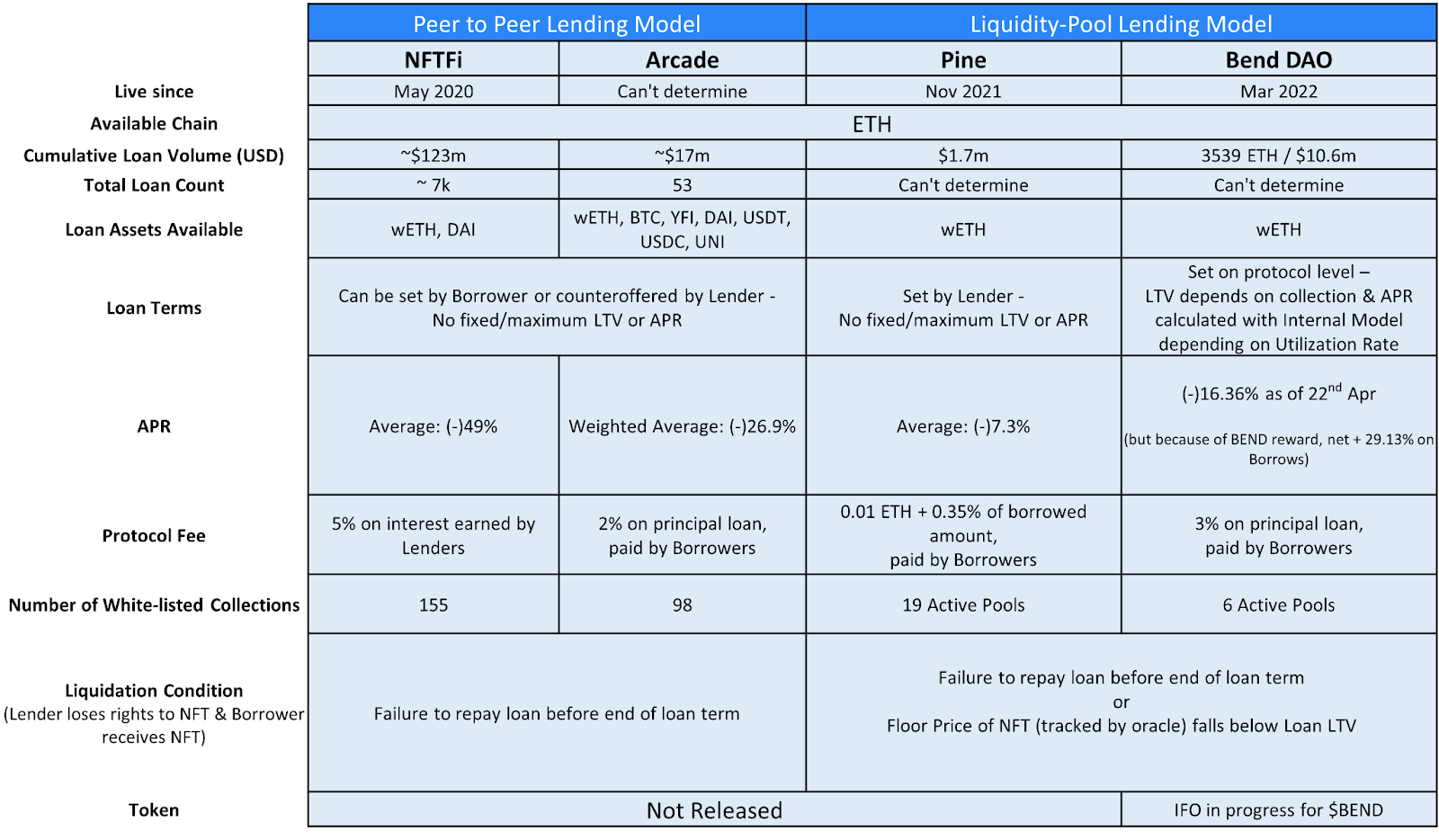

DeFi power users may wonder what trade offs NFTfi makes by employing a peer-to-peer versus a peer-to-pool model (e.g. Aave, Compound) model. Here are a few key trade offs that NFTfi made that we identified:

Con: Loan terms are bespoke, not set by protocol or lender (harder to scale liquidity fast)

Con: Slower matching as borrowers must wait for counteroffers, as opposed to borrowing from a pool

Pro: NFTs can have custom pricing, versus pool based models where NFTs are valued at collection’s floor price (via an oracle, which can also be faulty)

Pro: Borrowers can receive multiple offers from lenders with varying APRs / LTVs and choose whichever fits their liquidity needs best, vs. pool based models offering fixed terms

Pro: NFTfi as a platform does not underwrite any risk and is therefore less exposed to major market fluctuations than pool based models

Pro: NFTfi can scale in line with the overall NFT market across any vertical since it does not rely on algorithmic pricing, vs. pool-based models which can scale only as new pricing models get validated for new assets

3. Team

NFTfi currently has 15 team members, and is led by co-founder / CEO Stephen Young and co-founder Jonathan Gabler

Before NFTfi, Stephen was the Chief Product Officer at Coindirect.com and has spent most of his career building fintech solutions.

Jonathan joined NFTfi in July 2021, is also the co-founder of Token Engineering firm CADLabs and a previous McKinsey consultant.

4. Market Assessment

For clarity, there are currently two main forms of NFT lending protocols: ones that allow you to loan out your NFTs, and ones that allow you to collateralize your NFTs and borrow against them.

NFTfi focuses primarily on the latter and it is our view that the latter is likely to take off first due to a more generalizable value proposition for all NFT holders.

As of April 2022, the total market capitalization of ETH-based NFTs sits at ~$20 billion*. However, most of these values are illiquid, and NFTs sit idly in wallets. Illiquidity in NFTs is a major point of user friction as users are:

Unable to get immediate access to funding in times of emergency

Unable to access liquid funds without selling their NFTs

The market opportunity of unlocking NFT’s liquidity is essentially the entire $20 billion NFT market - and given current aggregate lending volume for NFTs represents ~0.5% of total NFT market, assuming a common 30% market penetration, there is approximately a 60x growth potential in the vertical alone without accounting for any growth in the NFT market.

* Based on NFTs from 2,250 collections on ETH network and its last transacted price. Find out more on NFTGo

** According to CoinGecko on 21st April*

5. Competitive Landscape

Below we examine a few protocols that compete with NFTfi and are currently live:

Note: JPEG’d is not listed above as the borrowing/lending functions are not live yet. Links to sources under Resources

Update as of April 28th: NFTfi has generated ~$150M in loans across ~8k loans

6. Catalysts

NFTfi currently has no live traded tokens. However, known upcoming catalysts include:

(Gradual roll-out since 4th April) V2 upgrade with functions like Unlimited duration loans, Pro-rata loans, Loans against ERC1155 & ERC998 NFT bundles, Loan extensions and renegotiations, Listings with binding terms and Loan obligation receipts

(TBA) Extension to other chains, starting with Flow Blockchain

(TBA) New financial agreement types due to protocol modularity

7. Thesis

Note that while currently NFTfi does not have a token, it is expected to launch soon based on the team’s V2 post. The following represents my own rationale for why I invested in NFTfi personally and is in no way an inducement to purchase any asset.

Currently, Aave has an annualized borrowing volume of ~$7.5B and trades at a $2.66B fully diluted valuation. At a $480M annualized borrowing volume (~$40M per month based on April’s volume), we project a $160M fully diluted valuation as a conservative floor for NFTfi before factoring in the platform’s impressive growth.

Note that this is a rough back-of-the-envelope calculation and does not factor in take rates or growth rates - the latter of which has been impressive for NFTfi: in March 2021, the platform generated $330K in loan volume; a year later that number was $27M, a whopping 80x annul growth with no token incentives.

The growth prospects for both NFT lending (with 0.25% of the activity compared to NFT trading) and NFTfi (market leader but only servicing ~1,000 unique borrowers, or 0.06% of users that have made at least 1 NFT trade on Opensea) are significant considering the nascency of both.

Potential risks from the NFTfi token lies in the complication of setting loan terms and having to wait for acceptance of loans, which might be a point of friction for onboarding. Users could end up preferring the convenience of liquidity pool models over the long term, which can curtail NFTi’s growth.

8. FAQs (Important snippets from the podcast)

Borrowers & reason for loans:

Mostly individuals but expecting more DAOs with NFT Treasury to participate

Take out loans to prevent liquidation on trading positions, take advantage of market opportunities (leverage trading, part of P2E game strategy and others) or pay for day-to-day stuff

Lenders & loan APR consideration:

Most Lenders are Liquidity Providing DAOs that run sophisticated strategies and bots

Lenders factor LTV, Volatility of NFT collection and Duration when planning their Lending strategies

Stephen expects Borrowers to have access to lower APRs over time and multiple competing offers from Lenders that run different strategies

Fundamental issues with LP model and why P2P is more suitable for NFTs:

LP models disregard NFT’s rarity and traits - NFT from the same collection are valued equally at floor price by an oracle. This is an issue for owners with rare NFTs since it limits their loan amount e.g floor CryptoPunk is 57 ETH but CryptoPunk with Alien traits are valued at > 2000 ETH

Unlike fungible tokens, there’s no guarantee that collectors will be able to buy back the same NFT once lost. Hence, liquidations triggered by falling floor prices are risky and puts unnecessary stress on Borrowers

P2P model does not face the above issues - NFT value is agreed between Borrower and Lender and liquidation is only triggered upon failure to repay before loan expiration

Counter-arguments to common criticisms of P2P model:

Longer waiting time compared to instantaneous loans with LP model

With Liquidity DAOs running automated strategies, NFTs from Top 20 collections typically receive 1 - 2 offers within an hour

Waiting time is expected to decrease with participation from more Lenders

LP model provides Lenders with yield for just depositing into a pool whereas yield depends on Loan execution with P2P model

Possible for Liquidity DAOs to allow individuals to buy into the DAO and earn a passive yield while the DAO manages the loans as a collective with more sophisticated strategies

10. Tips

If users are comfortable with smart contract risks, the protocol is live today and can be used. Users could:

Borrow - If your whitelisted NFTs are sitting idly in wallets and you need liquidity without selling your NFTs

Lend - If you have spare ETH/DAI and want to earn a yield on it

Rates users can roughly expect to pay / earn, for reference (subject to change).

11. Resources

NFTFi

Others

Links to full episode:

If you enjoyed this analysis and want to receive similar investment memos and research briefs, subscribe to Blockcrunch VIP today before prices go up by $1 next week:

DISCLAIMER

The Blockcrunch Podcast (“Blockcrunch”) is an educational resource intended for informational purposes only. Blockcrunch produces a weekly podcast and newsletter that routinely covers projects in Web 3 and may discuss assets that the host or its guests have financial exposure to. Views held by Blockcrunch’s guests are their own. None of Blockcrunch, its registered entity or any of its affiliated personnel are licensed to provide any type of financial advice, and nothing on Blockcrunch’s podcast, newsletter, website and social media should be construed as financial advice. Blockcrunch also receives compensation from its sponsor; sponsorship messages do not constitute financial advice or endorsement.

| A guest post by

|