E-Commerce in the Metaverse Age

Get in loser, we're going shopping in Decentraland

This research memo is for educational purposes only and not an inducement to invest in any asset. Subscribe to Blockcrunch VIP to receive in-depth project analysis, valuation models and exclusive AMAs.

Can We Make Money in the Metaverse?

Meta doesn’t rebrand its entire company and burn $1B a month on it if there’s no money to be made in the metaverse.

Citi estimates that the metaverse has a total addressable market of $8 trillion to $13 trillion, and will serve up to 5 billion users by 2030. Interestingly, out of all the activities, users are most excited to be able to shop in the metaverse. According to Mckinsey, commerce in the metaverse has the most significant potential economic impact of all use-cases and estimates a size of $2 trillion to $2.6 trillion by 2030.

These are big numbers to throw around for an industry that can barely agree on what “metaverse” even means!

This week, we’ll put those numbers to the test and evaluate the promise of commerce in the metaverse. For the purposes of this piece, we’ll assume “metaverse” refers to virtual, digital environments wherein users can explore and interact freely.

Contents

Examining Metaverses Today

Framework for Comparing Web 3 Metaverses

Commerce in the Metaverse Today

Key Developments Required for Mass Adoption

Examining Metaverses Today

The metaverse landscape today is nascent and broadly divided into 2 camps:

Web 2 metaverses like Roblox, where in-game assets (e.g. land, in-game items, characters) are all owned by a centralized entity

Web 3 metaverses like The Sandbox, where users own at least part of the assets via blockchain-based tokens, typically NFTs

Web 2 metaverses are mostly games with additional social elements, and are currently much further ahead than their Web 3 counterparts: Roblox has 220 million active users, which is more than 400x that of Sandbox and Decentraland combined!

Despite the nascency of Web 3 metaverses, major retail consumer brands have already struck partnerships with the two largest incumbents (The Sandbox and Decentraland) today.

The Sandbox

The Sandbox is a decentralized gaming ecosystem where creators can create, share and monetize assets and gaming experiences in a virtual metaverse.

Initially developed by game studio Pixowl as a Web 2 metaverse that allows users to craft their own universe by collecting resources like water, soil, sand and glass, the brand was acquired by prolific Web 3 investor Animoca Brands and re-developed into a Web 3 metaverse.

The Sandbox is one of the largest metaverse with over 2 million registered users and has onboarded over 200 partners to create themed lands and in-game assets, such as Gucci, Adidas, The Walking Dead and Standard Chartered Bank.

The Sandbox also created VoxEdit and Game Maker, two free software suites that allow brands and players to create voxel assets and experiences without coding knowledge. While this makes it easy to create Sandbox assets and experiences, creators should note that the custom program could limit the degree of interoperability with open-source standards and other metaverses.

The Sandbox had two rounds of alpha playtests but is currently not yet live to the public. Since the game is not live, the web-based marketplace is the primary facilitator of in-game assets transactions such as land, avatars, in-game equipment and cosmetic items.

It is unclear how and to what extent The Sandbox will facilitate commerce within the game, especially for physical goods, but the pipeline of notable consumer brands seem to signal interest, at least on the merchant side.

Decentraland

Decentraland is a browser-based virtual world platform, first opening to the public in February 2020.

Like The Sandbox, Decentraland allows creators to share and monetize their creations, with a weaker focus on in-world game experiences and a stronger focus on allowing its users to socialize. With a reported 300,0000 monthly active users, Decentraland is live and has already onboarded retail brands such as Nike, Atari, Coca-Cola and Samsung.

Unlike Sandbox, Decentraland accepts files created by 3rd party programs, which leads to a higher degree of interoperability with other metaverses. Decentraland’s web-based marketplace is the current primary facilitator of in-game asset transactions: to date, it processed 164,000 sales for a total volume of 350m $SAND ($377m in today’s $SAND price).

While the current in-game commerce infrastructure is a simple redirect to Decentraland’s marketplace or external links, Boson Protocol has integrated with Decentraland to allow users to shop for physical goods in-game.

Highstreet

")

Among the Web 3 metaverses with live tokens today, Highstreet is perhaps the one most focused on commerce as a primary go-to-market strategy.

Although Highstreet also focuses on its gaming experience as an MMORPG, they are positioned as a launchpad for retail brands to enter the metaverse space, with the intention of making the vast majority of in-game items products from real brands. For instance, Highstreet partnered with Buer Bear to sell 400 NFTs in-game, which are redeemable for physical merchandise in real life.

So far, Highstreet is the only metaverse with in-built infrastructure for in-game checkout and redemption of “phygital” (a mixture of physical and digital) items, and even have plans to integrate DeFi concepts like bonding curve to solve illiquidity issues. However, Highstreet is not yet live, so the effectiveness of their plans remains to be seen.

Framework for Comparing Web 3 Metaverses

In order for a Web 3 metaverse to support a full-fletched e-commerce ecosystem, it needs to:

be performant enough to support significant fluctuations in concurrent users;

have somewhat low friction for merchants to deploy storefronts;

have favorable fee structures for merchants, and finally;

have enough users to warrant merchant onboarding.

Below we compare the major Web 3 metaverses through this framework. The common thread seems to be the overall nascency of the entire sector: no single metaverse has over 400,000 monthly active users (compared to Roblox’s 50,000,000 DAILY active users):

Commerce in the Metaverse Today

While the emergence of a “Ready Player One” type metaverse with billions of concurrent users still seems like a pipe dream, brands are already recognizing the commercial potential of highly immersive virtual environments.

For instance, Gucci set up its Gucci Garden in Roblox last year and had more than 20 million players visit over the 2-week campaign. They also sold virtual Gucci purses for $6 each that resold for more than $4,000 (converted from their in-game currency Robux). Recently, one of China’s largest e-commerce giant, Alibaba announced their metaversal project that will allow shoppers to shop in virtual shopping venues with their avatars as well.

Perhaps unsurprisingly, we are beginning to see inklings of the first commercial use cases in Web 3 metaverses as well.

Metaverse Fashion Week

For example, Decentraland hosted the first-ever Metaverse Fashion Week in March with over 60 participating fashion brands like Dolce & Gabanna, Tommy Hilger and Phillip Plein. The event lasted for 4 days, and during this period, 108,000 unique visitors logged onto Decentraland. Though the figure does not represent all that attended the fashion event, it is a considerable bump in user activity considering their reported regular 300,000 monthly active users.

Users could immerse themselves in various fashion catwalks and after-parties during the event. Most importantly, users could browse from more than 500 new fashion pieces that were sold in the form of digital wearables (NFTs), physical apparel or both.

Snoopverse

Fashion brands aren’t the only ones extending their reach in the metaverse.

In late 2021, rapper Snoop Dogg partnered with Sandbox to build a metaverse experience dubbed the Snoopverse; one fan even paid $450,000 for a plot of land in Snoopverse. Snoop Dogg also released an NFT collection of 10,000 playable Sandbox avatars and access passes that granted fans access to exclusive NFT drops, his first metaverse concert and his parties in real life. Today, each avatar is worth $255 with a minimum collection value of $2.5 million, and access passes are reselling for $700.

Snoop Dogg’s entrance into the metaverse is a telling example of how brands can utilize metaverses to expand their reach and engage with the community.

Nike & CloneX

Another prominent example of a retail brand entering Web 3 metaverses is Nike. Last year, Nike acquired Web 3 native NFT studio RTFKT and launched NFT series CloneX.

At its peak, one of the 20,000 CloneXs was worth at least $60,000, valuing the minimum collection value at $1.2 billion. What started as a jpeg NFT has since expanded to in-game assets and avatars on Sandbox, customizable galleries in OnCyber, digital sneakers and a physical hoodie with augmented reality capabilities. Nike/RTFKT also kickstarted a creator economy, wherein CloneX owners own the commercial rights of their NFT and can create art, merchandise and brand with 3D files accessible by open-sourced programs.

What’s in store (no pun intended) for the future

To date, most of the commerce that occurs in Web 3 metaverses are for digital items, with uptake of NFTs that are redeemable for real world assets still quite low.

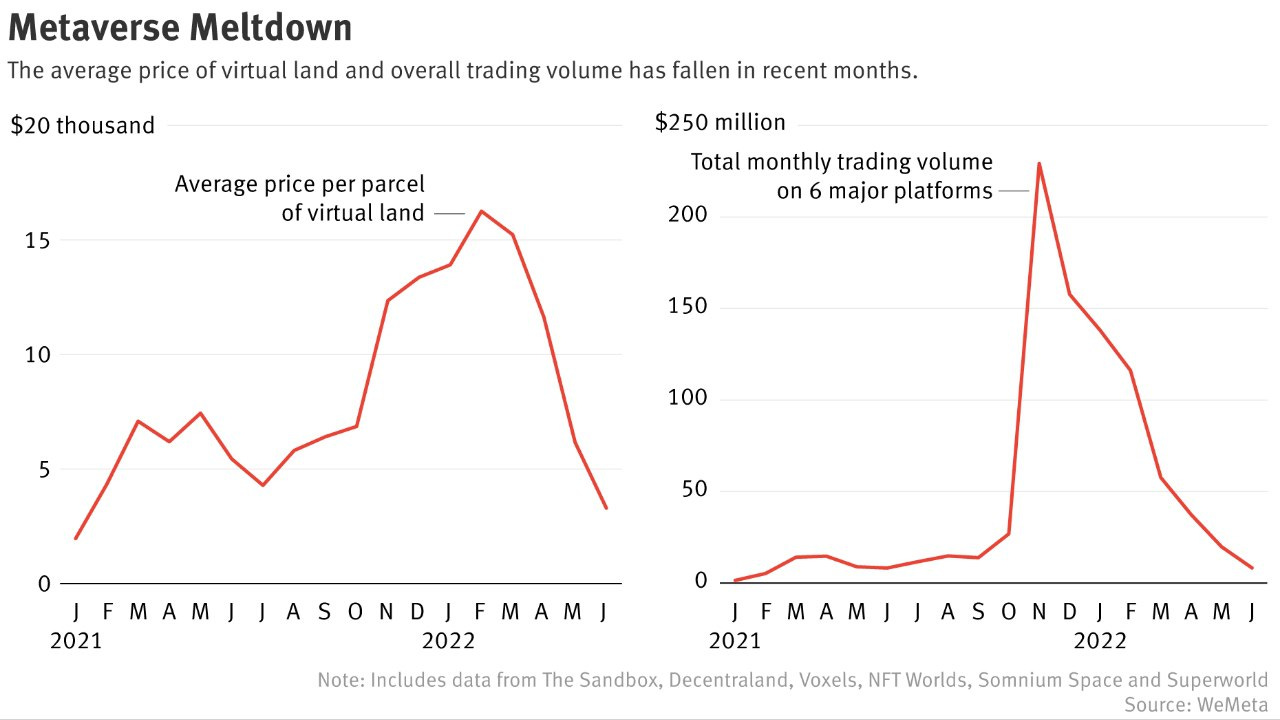

The digital asset that is perhaps the best proxy for general adoption for Web 3 metaverses is virtual real estate. To date, approximately $500 million has been invested into metaverse real estate. Notably, the average price per parcel of virtual land inflated and reached an all-time high of $16,000 after Facebook announced their name change last October.

Despite this apparent interest from major retail brands, Web 3 metaverse is facing a severe contraction in market size, wherein the current market-wide correction caused a more than 70% drop in virtual land price.

On the bright side, this provides brands looking to make their foray into the metaverse a cheaper cost of entry compared to a year ago. On top of the reduced cost of entry, the risk of metaverse expansion has also decreased as the metaverse space has developed and matured since.

This sentiment is reflected by capital inflow into metaverses. In the 1st half of 2022, over $120 billion has already flowed into the metaverse space – more than double the $57 billion in the whole of 2021.

However, the metaversal experience for commerce today is still in its rudimentary form. The following are a few key developments we believe need to occur to catalyze merchant adoption of Web 3 metaverses.

Inter-metaversal Interoperability

Currently, metaverses exist as individual applications with limited to no interoperability with each other: users can't bring their assets from one metaverse to another. Siloed metaverses are an issue for businesses as their investment is not only a bet on mass adoption of metaverses, but also on the success of that particular platform.

While it makes sense for specific in-game assets such as land, equipment and progress to remain siloed, we think cosmetic items/wearables and avatars should be made interoperable, allowing users to engage with the metaverse with one identity.

One of the projects focusing on building a common standard for metaverses is TreasureDAO (disclaimer: Jason is an investor). In addition, we see nascent efforts in promoting cross-metaverse interoperability amongst the incumbent players as well: Sandbox assets are now usable on OVER (an augmented reality metaverse) and Decentraland is launching Linked Wearables that allows existing NFT collections to launch their wearables in Decentraland without minting a new token.

Rather than waiting on metaverses to integrate with each other, projects like Ready Player Me and Genies also adopt a bottom-up approach to cross-game interoperability. Their avatar ecosystem allows brands to create only one instance of the asset (rather than multiple to adhere to different metaverse standards). Metaverses can simply integrate with Ready Player Me via their SDKs. For users, they just have to create an account with Ready Player Me and customize their avatar. After that, they can use the same avatar across 3,000 partner applications like Neos VR, Somnium Space, and Portal simply by signing in with their Player Ready Me account.

Device Compatibility

Most Web 3 metaverses have yet to launch on mobile because they are still optimizing the desktop experience, which is plagued with lag and the inability to handle the massive influx of users under one server.

We anticipate the roll-out of 5G, which is estimated to reach 4.4 billion users by 2027 and advancement in edge computing that promises lower latency than cloud computing to enhance user experience and enable device-agnostic access to the metaverse.

Seamless E-Commerce Integrations

Metaverse commerce is still highly experimental. For it to gain mass adoption, there needs to be more clarity on the operating procedures, interface and digital asset standards.

For example, during the most extensive test of metaverse commerce, the Metaverse Fashion Week in Decentraland, users complained that the shopping experience and interface were highly confusing and lacking. Some brands redirected users to their main e-commerce site, some linked to Decentraland’s marketplace, while others provided an interface with only basic product information. There is no de facto standard for approaching metaverse commerce's browsing and checkout process.

Furthermore, to redeem the physical equivalent of digital assets, different creators and platforms use different approaches when it comes to redeeming the physical equivalent of digital assets:

For metaverse commerce to be widely adopted, we believe that the browsing and checkout process should be contained within the metaverse. There should also be standardized guidelines for:

Differentiating physical-only and digital-only purchases

Redeeming the physical equivalent of the NFT

Clear expiration/cut-off date for redemption (or even remove expirations entirely)

Handling pre and post-redemption of the digital asset

As it stands, friction in metaverse commerce outweighs the benefits of shopping in the virtual space. When shopping in the metaverse is as seamless as e-commerce, we believe more brands and users will be onboarded and metaverse commerce can capture more market share.

Increased Immersiveness

Metaverse commerce experience today is still broadly similar to regular e-commerce because shoppers are interacting with the products over their flat 2D screens. We believe the metaverse commerce experience can be significantly enhanced with augmented reality (AR) and virtual reality (VR) technology.

The 3D environment of the metaverse, paired with virtual reality technology, opens up the possibility of an immersive experience that could even transcend physical retail. Augmented reality should achieve similar effects, albeit on a lesser scale than virtual reality.

We look forward to the future development of AR and VR devices that:

Further increases the convenience and access to AR and VR such as Snapchat’s AR Spectacles

Reduces cost of such devices, which is one of the primary reasons for lackluster VR adoption.

Summary

As online experiences trend towards immersiveness over time, we view the collision course between metaverses and e-commerce to be inevitable. What was once an experimental concept now has recognition from top retail brands globally, with an estimated impact of $2.7 trillion by 2030.

Notably, fashion and apparel brands, particularly luxury brands, are the first to establish partnerships with major Web 3 metaverse players, but are unlikely to be the last. Just as every major consumer brand has a social media strategy, it might be common for brands to have their metaverse strategy.

However, there exists significant headwinds to adoption - particularly for Web 3 native metaverses, namely lack of seamless commerce experience, lack of interopability and device compatibility, lack of privacy, and the nascency of enabling technologies such as VR and AR.

Today, web 2 metaverses like Roblox are taking the lead in terms of user base and development; however, we find the user-owned and open-source philosophy of Web 3 metaverses more congruent with the vision for an Amazon-scale virtual bazaar, and remain optimistic on what lies ahead.

DISCLAIMER

The Blockcrunch Podcast (“Blockcrunch”) is an educational resource intended for informational purposes only. Blockcrunch produces a weekly podcast and newsletter that routinely covers projects in Web 3 and may discuss assets that the host or its guests have financial exposure to. Views held by Blockcrunch’s guests are their own. None of Blockcrunch, its registered entity or any of its affiliated personnel are licensed to provide any type of financial advice, and nothing on Blockcrunch’s podcast, newsletter, website and social media should be construed as financial advice. Blockcrunch also receives compensation from its sponsor; sponsorship messages do not constitute financial advice or endorsement.

| A guest post by

|

Nice post Javier. And thanks for the @BosonProtocol mention.

We are launching Boson Protocol v2 in Oct with a much slicker UX and support for things like digital twins and multiple metaverses. Boson enable the sale of physical things as redeemable NFT, in a decentralized way.

Would love to have a chat about the v2 launch and the huge number partners we have lined up. Twitter @jbanon

Very informative post! Great to see a detailed dive into the variety of Web3 e-commerce projects out there.